It is only possible to pay interest only on your mortgage for a limited period of time, usually up to the first five years.

Your repayments will then revert to principal and interest repayments for the remaining loan term.

The catch is that the full balance now must be repayed in a shorter time window, which can lead to a sharp increase in the repayment amount and a shock to the household budget!

Sound like a daunting prospect? The good news is there are alternative options to just copping the higher payments.

In this article, we will discuss all of your options at the end of an interest only period so you can find the most suitable outcome for your circumstances.

Common Interest Only Scenarios

Interest-only (IO) loans are a tool that are most commonly used by the following groups:

- First home buyers (FHB) who need flexibility in their household budget early in their property ownership journey.

- Investors who are looking to maximise their tax deductions and optimise cashflow to support their portfolio.

We will work through each scenario below through the lens of these two groups so you have some context for how each outcome works in practice.

A key difference is that the circumstances of the FHB are likely to change over time. Whereas the motivations of some investors will not.

Your Options When Your Interest-Only Term Ends

Below are five options for what to do at the end of your interest only term.

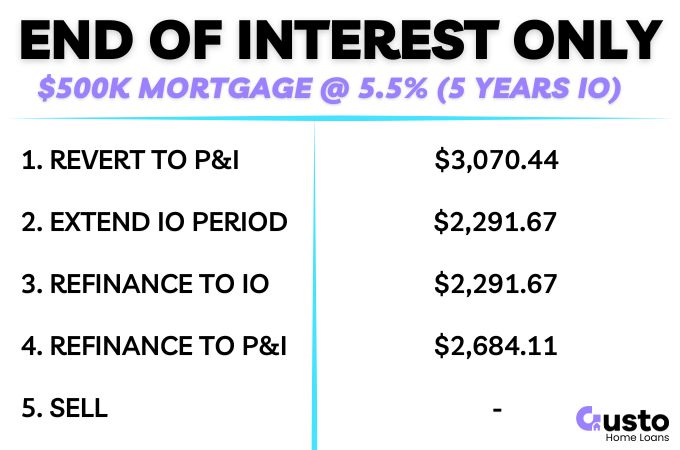

For the purpose of the examples, we will assume a $500,000 (@ 5.5% interest) mortgage to be repaid over a 30 year term, and a five year IO period that is expiring soon.

Option 1: Revert to Principal & Interest (P&I) Repayments

The default option is to do nothing and at the end of your 5 year IO period your repayments will adjust to the required amount to repay the principal balance over the remaining 25 years.

On a $500,000 mortgage the IO repayments would be $2,291.67 per month for that first 5 years.

However, the P&I repayment will be $3,070.44 for the remaining 25 years. An increase of $778.77.

First Home Buyer

Over the initial five years, first home buyers will often progress in their careers and their household income will have increased.

So it may be feasible to manage the higher repayments.

The benefit of this option is it is the fastest pathway to becoming debt free.

An aggressive repayment schedule will drive the debt down quickly and repay the full amouht in 25 years.

However, if the household budget remains tight then it may be too strenuous to commit to the higher repayments.

Investor

The rent an investor is collecting on an investment property may have increased sufficiently to cover the increased P&I repayments.

If they choose to direct the additional cash flow to repaying the debt then they will own the asset mortgage free in 25 years.

However, over time the tax deductable interest will reduce and their tax bill will increase year on year all things being equal.

Option 2: Extend the Interest-Only Period

Some lenders will allow you to simply extend the IO period for another set period, subject to meeting thier criteria.

If you need to preserve the IO repayments then this can be the path of least resistance.

However, not all lenders will consider this due to the amplified impact on repayments at the end of the subsequent IO period.

For example, if you secure another two years of IO payments then your repayments will increase from $2,291.67 to $3,196.44 over the remaining 23 years.

First Home Buyer

This option makes the most sense if there is an upcoming change in household budget expected, but is too far away to take on the higher repayments now.

For example, a young family may have children currently in childcare (which is bloody expensive!!).

If they will be transitioning to school in 18 months time there will be a signifcant reduction in their expenses at that time.

Until then, it could make sense to stick with the IO mortgage payments until that financial relief comes.

Investor

If an investor is planning to sell the property within the next year or two years then minimising the repayments for the immediate future could be a priority.

However, an investor who is looking to expand their portfolio in the near future could find the looming prospect of much higher repayments an obstacle to obtaining future finance.

Option 3: Refinance to Another Interest-Only Loan

To avoid the pressure cooker of Option 2 you could refinance your loan to reset that 30 year term, with another IO period to start.

This has a number of advantages for all groups:

- You can seek out the best current mortgage deals in the market and potentially reduce your repayments.

- You can select an IO period that is most suitable to your current needs.

First Home Buyer

The freedom to select from a broader range of IO terms can allow you to align your repayments with expected life events that will affect your household budget.

You can also secure the lowest possible minimum repayments for now, and make additional repayments as your circumstances allow.

This is the most flexible option but will also cost the most over the long run.

Investor

This will enable you to preserve the maximum tax deductible interest amount well into the future.

You may also claim the costs associated with refinancing your mortgage. But as always, consult with a tax professional for personal advice.

Option 4: Refinance to a New Principal & Interest Loan

If you are ready to start paying down the debt it often makes sense to refinance your loan.

The mortgage market is very competitive and there may be opportunities to save thousands of dollars in costs by doing so.

In this scenario, you can:

- Retain the 25 year repayment period and move to the most competitive product offering on the market to maximise your savings.

- Reset the 30 year repayment term to keep your P&I repayments manageable, and move to the best option in the market for your circumstances.

First Home Buyer

You may be surprised just how little your repayments change when moving to P&I repayments as an owner occupier.

P&I loans for this group generally attract some of the lowest interest rates on the market.

By also resetting your loan term to 30 years your minimum repayments will be far more manageable.

| Monthly Repayments | Interest Only | Principal & Interest |

|---|---|---|

| Current (5.5%) | $2,291.67 | $3,070.44 (25 Years) |

| Refinance (5.0%) | – | $2,684.11 (30 Years) |

Repayments have only increased by $392.44 per month compared to the existing IO loan (that is coming to an end) and you are on the pathway to repaying the debt and building equity over time.

If you can secure more favourable terms AND reduce your interest bill at the same time then it is a big win all round!

Investor

An investor that is content with their portfolio may switch focus from cash flow preservation to repaying debt.

By extending the loan term to 30 years and seeking a reduced interst rate, the burden of repayments can be minimised.

Each rental increase can further reduce that burden or accelerate the repayments so that retirement date that be achieved faster.

Option 5: Sell the Property

You have have planned all along to sell the property prior to the end of the IO period. If that is the case then all is going to plan and no change is needed.

However, if the prospect of higher repayments at the end of the IO period is just too much for your circumstances then selling may be the option of last resort.

First Home Buyer

While it may be dissapointing to sell in response to the higher repayments, this does not have to mean your home ownership dreams are over.

If the value of your home has increased over the five year period you may have a large cash deposit you can put towards your next purchase.

You can then aim for a price point where you know your mortgage repayments will be manageable long into the future.

Investor

Even a forced sale can be a huge opportunity for the investor. Once the equity is turned into cash you can find that next investment opportunity.

The investor has the advantage of not being tied to a particular area or property type. So they can setup their next investment to suit them based on a number of variables, such as:

- A higher yielding asset (more rent) so that a similarly priced property requires less out of pocket cash to meet repaymehts (if any).

- A higher growth area, and just return to the interest only repayments while the growth plays out.

The possibilities are endless which is what can make property investment so much fun! Even after an investment turns pear shaped.

Conclusion

The most important thing is to be aware of when your interest only term is coming to an end so you can engage wth your broker early on.

These dates can really sneak up on you! And if you are not prepared then you risk missing a repayment which could limit your options if you do choose to refinance.

If you are still not sure what the right move is for you then click below to get in touch with the team at Gusto Home Loans.

We will conduct an obligation free health check on your current mortgage so you know what options are available to you.