Despite the digitisation of the lending industry the timeframe to approve a home loan application has not improved much over the past decade.

However, there are some lenders who are clear leaders with their processing times and regularly produce same day conditional loan approvals on complete applications.

The real time suck often comes before and after the actual assessment – generating a complete loan application, and satisfying the approval conditions.

In this article, we will discuss each of these elements so you understand the full process so you are never caught out with a finance clause that is unrealistically short!

Plan for the Slowest Loan Approval Timeframe

When submitting an offer to buy property you should always include a finance clause so that if your loan is rejected you can walk away from the purchase without penalty.

You should also give yourself sufficient time to get that approval locked down before it expires.

There is nothing worse than doing all the work to get an approval, only to have your request for an extension denied by the vendor and the sale contract cancelled.

You will then have to start from scratch on both the house hunting and the loan application.

So, hope for the best but plan for the worst.

The vast majority of approvals can be secured in 10 days, but you should request at least 14 days upfront so you have a buffer to work with.

While you could aim for 21 days, you also don’t want to make your offer unappealing to the vendor compared to others.

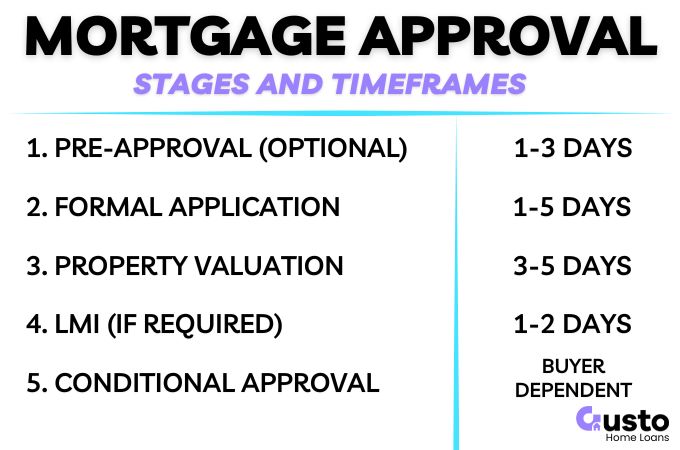

Home Loan Approval Stages and Timeframes

Here is a brief summary of each step towards an unconditional loan approval.

Not every step will be necessary in all circumstances and the process can be somewhat faster when the information is complete, the property is simple, and the loan to value ratio is small.

It is also worth noting that a mortgage broker may be able to hurry things along when there are exceptional circumstances.

The team at Gusto have working relationships with a number of lenders and can give things a nudge along if there is a deadline approaching.

Home Loan Pre-Approval (1-3 days)

This step is optional and often completed so that a buyer has some guidance for what their budget is prior to starting their hunt.

A pre-approval will consider your income, expenses, other debts, and your credit history to provide an indicative approval up to a set amount.

However, this is only part of a full mortgage assessment. The most important element is still missing – the asset being purchased.

Until there is a contract of sale and an asset to assess the pre-approval is generally saying “we will probably lend you this much, if we also agree the property is acceptable security.”

Given the low commitment from the lender to follow through on this the are much faster to turnaround.

The biggest hold up is likely to be incomplete documentation on your part rather than the speed of the lender.

Formal Mortgage Application (1-5 Days)

Now that you have a Contract of Sale, and hopefully a finance clause, the clock is now ticking to get your unconditional loan approval.

If you have completed the pre-approval then your part is well advanced. You may only have to update any financial information that has changed since the pre-approval, and possibly supply your most recent payslip.

If you skipped the pre-approval then there is not a moment to waste when collating all of your documents (it can be a lot!).

Once your documentation is complete the lender can start their assessment.

Some efficient banks, and modern non-bank lenders, can turn around a credit assessment in quick time but it does fluctuate depending on their workload on any given day.

The lender will run through the following:

- Checking your credit history to ensure your score meets their criteria, and there have been no adverse credit events.

- Verifying your income either through the provided documentation or contacting your employer.

- Calculating your debts and living expenses to ensure you can afford your repayments.

- Assessing the property against internal criteria to ensure it is acceptable security.

- Verifying you have the funds to complete the transaction, including the deposit and your closing costs (stamp duty and other fees).

- Calculating the required loan amount compared to the selling price (and subsequent valuation) to ensure it is within their internal limits, and if Lenders Mortgage Insurance is required.

As you can see, this is far more comprehensive then the pre-approval process so in most cases it takes a little longer.

There is still one missing piece of the puzzle that is often out of the lender’s hands, but is critical to getting that final approval.

Property Valuation (3-5 Days)

A property valuation is usually carried out by an independent third party valuer and can sometimes be a cause of delay.

Especially when site access is required and you have a less cooperative seller, or worse, uncoopertaive tenants that are yet to vacate!

The best case scenario is the lender accepts a Desktop Valuation. This is quick and easy for the valuer to produce.

However, an on-site valuation is the norm and will require the vendor and selling agent to assist in providing access as soon as possible.

As long as the valuation comes in at, or above, the selling price then this should not be the caise of any complications or delays with your applicaiton.

Lenders Mortgage Insurance (LMI) Application (1-2 Days)

If you are borrowing more than 80% of the purchase price then you may be subject to LMI.

While this should not delay the approval process by much, if at all, it is worth noting that there are more steps to complete in this circumstance.

Conditional Approval (Situation Dependent)

After all of the previous steps are completed there may still be some additional requirements from the lender unique to your circumstances.

The time to complete these and secure unconditional approval depends entirely on how fast you can tick off each condition.

Some examples may include:

- Closing down a credit card account to reduce your overall debt or accessible credit limit.

- Providing an up to date rental appraisal on a property.

- TBD

And once you secure that final approval you can proceed to an unconditional contract of sale and look ahead to the settlement date in 4-6 weeks time (depending on your state).

Conclusion

We always encourage our customers to seek out a pre-approval prior to placing offers on any property they are interested in.

Aside from having a strong indication of your budget you can also identify any gaps in your documentation without the time pressure that comes with a contract of sale.

With large sums of money at stake, lenders will be very particular with the documents they require and it is best to address these early.

It will save you stress, and give you more confidence in achieving a fast home loan approval when it really counts!

As always, the team at Gusto is here to guide you through the whole process. So click below for an obligation free consultation.