With housing affordability a constant headline for the past 20 years it was only a matter of time until mortgage timeframes were extended to 40 years.

In the past 12 months, multiple lenders have come to the market this new 4 decade loan product.

Some feel like this is going too far and is a bad idea!

While it sounds daunting to take on a financial commitment that is half the average lifespan, the reality is that very few people will pay these off over the full term.

In this article, we will discuss the potential costs over the long term and how to use this product to your advantage.

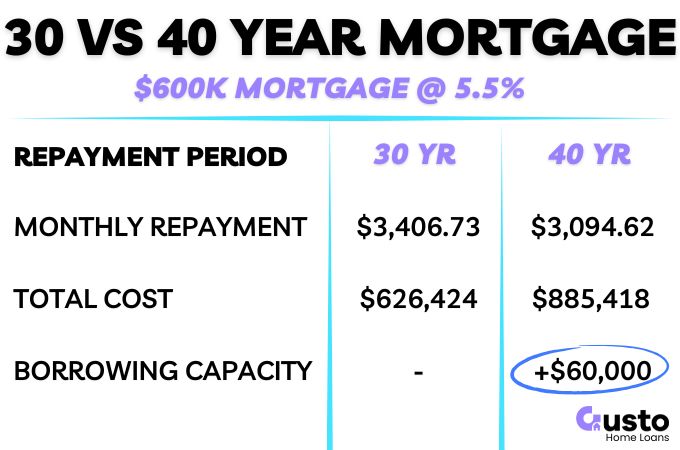

30 vs 40-Year Mortgage Cost Comparison

The primary benefit of the longer term mortgage is the lower minimum repayment required to service the loan.

This may provide access to the housing market for those who have just not been able to borrow enough in the past.

However, even with a 30 year loan, the portion of your repayments that actually pay off the principal is very low.

So let’s see how beneficial this is for the prospective home owner.

For the purpose of this example, let’s consider a $600,000 mortgage at 5.5% interest.

Monthly Repayments

The repayments on a 40 year loan term are $312.11 per month lower than the 30 year mortgage, or just over $70 per week.

| Term | Monthly Repayments |

|---|---|

| 30 Years | $3,406.73 |

| 40 Years | $3,094.62 |

The reduction can make a world of difference for borrowers juggling other financial commitments and are on a tight budget.

However, your capacity to repay a mortgage is assessed at a much higher interest rate than what you actually pay one day one.

Plus most lenders have additional buffers for surplus cash even after the higher rate is applied.

Things are unlikely to be this tight for most borrowers for that extra few hundred dollars to really matter.

A far greater incentive could be the potential for a higher borrowing limit overall.

Increased Loan Size

Every lender has a different formula for calculating your maximum borrowings.

But as a general guide, the additional $312.11 a month over an additional 10 year period could increase the maximum mortgage size by around $60,000!

This could make a material difference to the quality of house you can afford to buy, or the suburb you wish to buy in.

If you would like an accurate calculation on your borrowing capacity then get in touch with our expert team below.

Total cost

This all sounds great so far, but of course there is a catch!

If you do repay the 40 year loan over the full term then the cost is going to be much higher.

Over the extra 10 years you will repay an additional $258,994.17 in extra costs. That is a massive 41% increase in the overall cost of your mortgage!

| Term | Total Interest Paid |

|---|---|

| 30 Years | $626,424.24 |

| 40 Years | $885,418.41 |

The chances are that over 40 years your financial circumstances will change considerably.

Your earnings may increase over time making it possible to gradually increase your repayments and accelerate that repayment trajectory.

How to Make a 40 Year Mortgage Work For You

Your level of financial discipline is one of the most significant factors in whether a longer loan term is suitable for you.

So lets use this as a criteria for how best use this financial tool. You may have to be very honest with yourself for where you fit on the spectrum.

Strong Financial Discipline

Keeping your minimum repayment as low as possible allows flexibility in your household budget and you will be able to better handle unexpected expenses.

You can always make additional repayments on your loan, or accumulate a savings balance in an offset account to reduce your interest bill.

This gives you the best of both worlds, but only if you stick with it long term.

Lower Financial Discipline (But Needs a 40 Year Term)

If you need to borrow that little bit extra to get into the property market then you may need a 40 year loan upfront to get that access.

However, as your situation changes you may consider refinancing to a shorter loan term.

As you can afford higher repayments you can increase your minimum commitment so that no matter what else you do with your finances you are paying down your debt as quickly as you can manage.

Without having to rely on willpower.

Lower Financial Discipline (And Sufficient Capacity)

If you are earning enough to afford the property you desire comfortably then there is less need to play it safe with conservative minimum payments.

For someone who struggles to save consistently, or the pile of cash in an offset account is just too tempting, then a shorter loan term may be best.

Think of a 25 or 30 year loan term as a method of forced savings that will benefit you tremendously over the long term as you grow your equity.

Pros and Cons of the 40 Year Home Loan

Below is a short summary of the reasons for and against the 40 year mortgage.

Whether it is suitable for you depends on your stage of life, and long term objectives for the property.

Advantages

- Affordability – A longer loan term means lower minimum repayments and a more affordable mortgage.

- Flexibility – You will retain more choice for how you distribute your income. You can pay extra to reduce your interest bill, or manage other expenses as they arise.

- Borrowing capacity – The higher potential borrowings could help you into a better property or suburb than you could otherwise afford.

Disadvantages

- Total cost – If you repay over the full term you will pay approximately 40% more in interest over the life of the loan.

- Slower equity growth – You will pay down the principal much slower and it will take longer to build up significant equity.

- Time – An additional 10 years of repayments is a significant burden to carry if you do no make additional repayments or refinance.

Inflation and Asset Prices

Once you own a property then time is generally your friend.

Even if your earnings only increase at the pace of inflation for the next 40 years you will find that today’s repayment amount will seem very cheap in the second half of that loan term.

Allowing you to either increase repayments and pay the loan off faster, or preserve your increasing level of disposable income.

Let’s consider an example for a couple who are both earning the median salary in Australia of $67,600.

If they both receive annual pay increases of 2.5% (mid point of the RBA’s inflation target) then in 30 years time they will both be earning $141,795.

So what impact will this have on their budget for the last 10 years of their 40 year mortgage?

Let’s also assume that interest rates and the PAYG tax system stays the same – making this a worst case scenario from a tax point of view.

| Timefram | Household Income | Repayments | % of After Tax Income |

|---|---|---|---|

| Today | $135,200 | $3,406.73 | 37.1% |

| In 30 Years | $283,590 | $3,406.73 | 19.4% |

As you can see the repayment burden reduces significantly.

After 30 years the surplus income after making the mortgage repayment increases from $5,779.93 to $14,115.77.

You could really crush the remaining balance on the loan in quick time if you choose to do so.

Conclusion

A 40 year mortgage sounds scary at first!

But if you understand how to use it to your advantage it presents an exciting opportunity to accelerate, or heighten, where you can enter the property market.

With price increases in most major cities unlikely to slow down much over the coming decade then utlising the 40 year mortgage could give you an edge over those who shy away from it.

If you would like to know more about your borrowing capacity and what rates are available to you now then get in touch with the team below.