The mortgage market has long been dominated by the major banks in Australia.

But the emergence of second tier lenders has introduced much needed competition, and has generated increasingly superior consumer outcomes.

Despite this, some still shy away from a lender they have never heard of. Even if they can offer a better deal.

Most of this hesitancy is unfounded with Australian financial regulations amongst the strictest anywhere in the world.

So the focus should be more on where to get the most suitable mortgage for my circumstances, and future objectives.

In this article, we will discuss the differences between each type of mortgage lender and conduct a detailed comparison between the banks and non-bank lenders.

Why Big Bank Home Loans Are Unique

The largest five banks are responsible for approximately 70% of all mortgages in Australia and play an outsized role in the general health of the economy.

As a result, there is a lot of regulatory oversight to control the risk of these large institutions.

Lending is generally regulated by ASIC and all credit license holders fall under their purview.

However, Australia’s banks are also subject to regulations from the Australian Prudential Regulatory Authority (APRA).

For all us regular folk, this is usually pretty meaningless.

However, in November 2021 APRA implemented a big change that created a divide in consumer outcomes between bank and non-bank mortgages.

Mandatory Servicing Buffer

In the leadup to this change the housing market was surging on the back of record low interest rates.

There was an increasing risk that a reversion to normal rates in the future could place significant stress on the loan books of the major banks.

Large scale defaults, equals big trouble for the economy… America’s GFC experience being an extreme example.

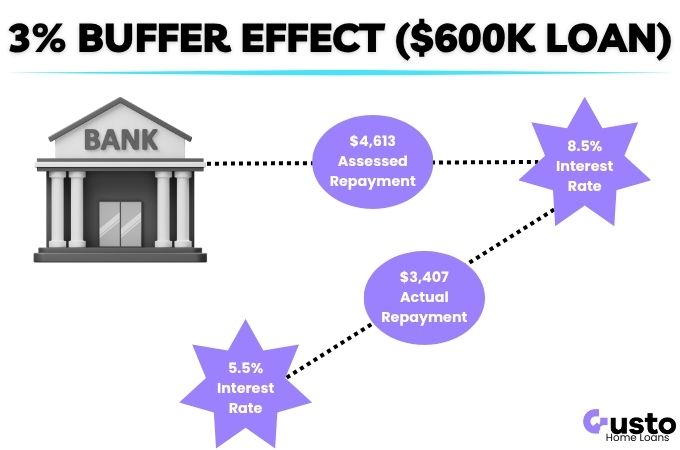

So, to limit future risk APRA imposed a mandatory 3% buffer to be added to the interest rates used to assess a borrower’s repayment capacity.

And this has remained in place throughout the steep rate increases that have been seen since.

If you apply for a mortgage through a bank today you are going to be assessed at an 8%+ interest rate.

Which will significantly reduce your maximum borrowing amount.

Funding from Deposits

The other major difference is that a bank has the freedom to fund part of their loan book through customer deposits held on their books.

This is a huge advantage for them as it is a low cost funding source compared to alternatives.

However, the government also guarantees deposits up to $250,000 and would be responsible in the event of a major bank failure.

So they are watched closely by the regulators, and have limited freedom to pursue flexible and creative solutions for their customers.

Public Relations

The last major difference is the reputational risk to a bank for everything that they do.

From Royal Commissions, to Senate hearings, and court cases, it is not uncommon for banking executives to be put on show to justify their organisations decisions.

So their risk appetite on this measure alone is very different from a second tier lender.

This leaves a lot of gaps in the market for smart operators to provide superior solutions.

The Role of Second Tier Lenders

Second-tier lenders, or non-bank lenders, have created much needed competition in the market to keep things fair for consumers.

While also broadening the range of mortgage products available to survey various niches that the banks are not interested in.

They do not have access to deposits to fund their loans which allows them to operate differently to the banks, and can lend without the same level of risk associated with the whole financial system.

No APRA Regulations

Non-bank lenders are not required to assess a customer’s repayment capacity using the mandatory 3% buffer mentioned earlier.

They still use similar buffers as part of their credit policy, but this is an internal risk control rather than an economic risk imposed on them.

As a result, you will get a range of potential outcomes depending on which non-bank lender you apply with.

We will share some examples later in the article.

Agile and Flexible

Without the weight of big-bank bureaucracy, these lenders can be more agile and responsive. They tend to tailor solutions for borrowers who fall outside traditional credit policies — such as the self-employed, those with minor credit issues, or people with unconventional income streams.

Niche Specialisation

Given the number of second tier lenders that are competing for market share, you will find that they often target a specific market segment.

Some examples include:

- Self-employed borrowers who find it hard to evidence regular income.

- Borrowers who earn a significant portion of their income in bonuses or overtime.

- Borrowers with a very low risk of default (lots of equity and a blue ribbon capital city property).

The list goes on… The good news is that if you fit into one of these niches you can secure a much better deal than what you may get at a major bank.

Comparison of Big Banks vs 2nd Tier Lenders

The comparison below will focus on a number of key elements of mortgage products and the application process.

The importance of each element will differ for everyone. So as you read through you should take note of what you care about most before deciding what mortgage provider makes sense for you.

If you would rather leave it to the experts, then click below to speak to our expert team!

We can do all the legwork for you and find the best deal that is most relevant to your objectives.

Interest Rates

While the headline rate is what draws people in, what you should really pay attention to is the comparison rate.

This is intended to capture the full cost of a loan, inclusive of fees.

Big banks often cite a low interest rate, but it is only available through a professional package that costs a few hundred dollars a year to access.

While this can be great for those with multiple mortgages, you always have to weigh up whether this makes sense for your situation.

Depending on the type of 2nd tier lender, you will get a much broader range of interest rates.

This will mostly depend on the risk profile of the target customer.

A low risk customer will often qualify for a rate lower than what could be obtained through a bank.

If we compare two of the examples given earlier:

- Higher rates – lender specialising in self employed mortgages.

- Lower rates – lender specialising in blue ribbon city properties with a low loan to value ratio.

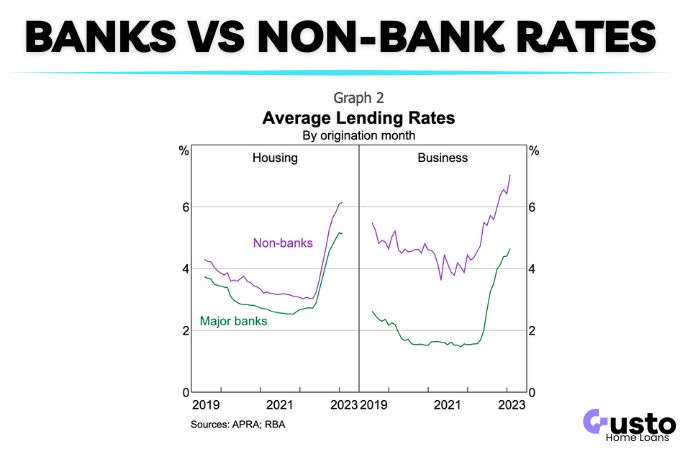

Having said that, on average banks are able to offer lower interest rates due to their lower funding costs and limited risk appetite.

This will be skewed by the variety of non-bank loans on offer that are targeted towards higher risk customer segments.

The important question is where can YOU get the best rate.

Speed of Credit Assessment

When you think of a big bank, you think rigid processes, layers of bureaucracy, and inflexible regulation.

But not all banks are created equal. In fact, Macquarie Bank especially have a market leading platform and response times.

Others are a bit more old-school.

However, if we are judging a whole category as one collective then non-bank lenders often excel at digitised and efficient processes that can turnaround decisions quickly and fast approvals are possible.

Speed and service is often a big selling point of these lenders.

Credit Criteria and Borrowing Power

As we have covered, the big banks are unlikely to offer the most favourable borrowing power assessment.

If your repayments are assessed at 8-9% it can severely inhibit your ability to finance your dream home!

Consider a basic example where someone is assessed at 8% at a bank vs 6.5% at a non-bank lender.

For simplicity we will assumed a $100k annual salary, no other debts, kids, and average living expenses.

The difference in borrowing power is as much as ~$93,000 based on this factor alone:

- Bank: $694,000

- 2nd Tier Lender: $787,000

Second-tier lenders also have more flexible credit models that can be surprisingly accommodating.

For example, if you bonus income is a big part of your annual salary then a bank may only consider 50% towards your assessable earnings.

Whereas some non-bank lenders will count 100% of these earnings!

Adding another $ to your borrowing capacity.

Product Range

A banks is able to provide an extensive range of loan types, financial products, and associated services.

If you prefer to do all your banking in one place then you can get great value with some banks.

Need multiple offset accounts? A low rate credit card? Or financial advice as part of a comprehensive financial planning solution?

The banks can do it all!

If you just need a mortgage with some basic features then you may get a better deal at a second tier lender.

Customer Experience

Your best option here depends on what you value in your customer experience.

Bank branches still exist (for now), so if you like talking face to face then a bank is where you can get this experience.

If you prefer to deal with everything online and drive the process yourself, then non-banks will be a better choice.

You can get the best of both worlds by using a broker of course, while having full flexibility over the lender you select.

But that is another topic altogether.

Technology & User Experience

While some non-bank lenders are positioned as leaders in fintech and have slick interfaces for their application forms, I have found the actual process of completing to not vary that much.

In fact, some are downright frustrating.

A certain online lender has an application that is a conversation with a chatbot. Which makes it very difficult to revise information in a more complex application.

If you have multiple investment properties, or any kind of complex financial information to convey it can be inflexible.

The least gruelling app form that I have encountered is in fact our own with a range of convenient features to make it as easy as possible. Check it out below:

Post approval is where the user experience can really matter.

Your netbanking portal and banking apps could be your companion for up to 30 years!

All but one major bank do a very good job of net and app based banking.

Whereas it can be hit or miss with non-bank lenders. However, with less functionality required it just doesn’t matter in most cases.

Brand Trust and Reputation

While some may prefer dealing with a large banking institution that they are familiar with, there are few genuinely practical reasons for this.

Australia is a heavily regulated lending market with layers of consumer protection in place.

Especially around how financial hardship and account delinquency is handled.

The mortgage market is so competitive that you are going to be treated well no matter where you go.

Is It Safe to Get a Mortgage with a Small Lender?

Yes, it is safe to get a mortgage with a small, unknown lender, as long as they hold an Australian Credit License (ACL).

There are strict regulatory guidelines that are policed by ASIC. Failure to uphold standards can result in heavy penalties and a loss of license.

All mortgage lenders will display the details of their ACL on their website.

What Happens if the Lender Goes Bust?

The chances of an Australian mortgage lender going bust is very slim.

As we saw in the pandemic years, the government will make big moves to prevent any type of broad system failure in the financial system.

However, if an individual lender goes into liquidation then the mortgage assets will be sold to another party.

You would continue to make your payments without interruption and the mortgage contract would remain in-tact.

The only recent example where a lender came close was the Westpac acquisition of RAMS Home Loans in the aftermath of the GFC back in 2009.

The brand was acquired and bankruptcy was avoided. The existing mortgages were not included in the sale and were left to “run-off” over time.

Summary – Why Choose a Big Bank

- You have more complex financial needs or financial structures that a large bank can accommodate.

- You would like access to associated products, such as a credit card, that are provided as part of an all-in-one solution.

- You have multiple mortgages and would benefit sufficiently from the discounts available through a “professional package”.

- You prefer all of your banking to be done in one place.

Summary – Why Choose a 2nd Tier Lender

- You want the best interest rate possible and qualify for a low cost lender.

- A large portion of your income is from bonuses or overtime, and you need to maximise your maximum allowable borrowing limit.

- More flexible mortgage solutions are available to suit your circumstances. You may find a non-bank lender that specialises in that area.

- If you can refinance to a cheaper, or more suitable, mortgage product.

Conclusion

Second tier lenders provide important diversity of mortgage solutions and additional competitive pressure on the big banks.

Since they have emerged in the market, consumer outcomes have improved significantly.

Any preference for a familiar banking name just for the sake of it is outdated thinking and will lead to an inferior result.

If you would like a free consultation to determine if you are best suited to a large bank or a second tier lender then get in touch below.

You may be surprised how good some of the mortgage deals available are.