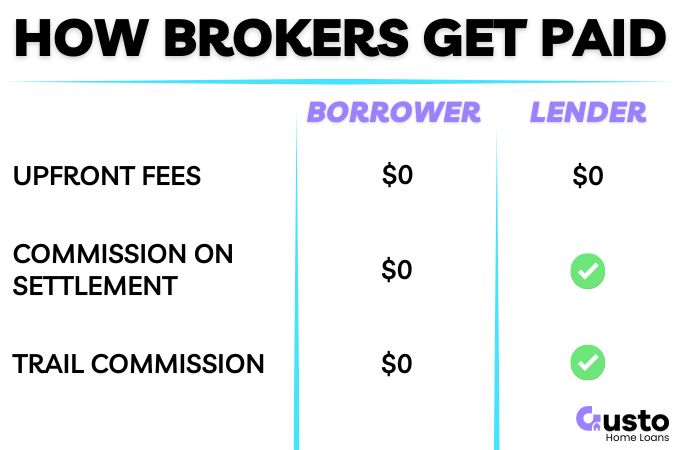

Most Australians do not have to pay a mortgage broker anything for their services.

Lenders pay an upfront commission on settlement of a new mortgage, plus a small ongoing commission for the life of the loan.

However, there are occasions where an upfront fee is required by the broker that is paid by the borrower.

In this article, we will discuss the standard payment system for a broker that applies to your everyday borrower and the more complex exceptions that attract a fee.

The Role of a Mortgage Broker

A mortgage broker will manage the home loan application process from initial assessment through to settlement.

Typical services include:

- Calculating your borrowing power and serviceability positioning.

- Selecting the most competitive mortgage solution for your situation.

- Packaging your application to meet strict lender criteria.

- Chasing up valuations and credit assessors to minimise delays.

All of which requires a significant time investment, but how do they get paid for the work they do?

The answer is usually by the lender they place the loan with.

How Mortgage Brokers Get Paid

In most residential loans, the lender pays the broker’s fee at settlement.

Banks view this as a distribution cost and is often cheaper than maintaining a massive network of branches and salaried staff.

Remuneration generally falls into two categories:

Upfront Commission

This is a one-off payment from the lender at settlement and typically ranges between 0.60% and 0.70% of the loan amount + GST.

It is based on the drawn amount, not the limit. So, if you are approved for $800k but only draw $500k, the broker is paid on the $500k.

Trail Commission

An ongoing payment to incentivize the broker to support you long-term.

This usually ranges from 0.15% to 0.25% per annum, calculated on your outstanding balance.

As you pay down the debt, the broker earns less.

What This Means For You

You do not pay the broker separately for a regular residential mortgage.

There is no additional invoice to pay, and 100% of your mortgage repayments go to the lender.

Does commission mean a higher interest rate?

Generally, no. Commissions are a marketing cost for the lender.

However, some of the major banks have recently introduced discounted rates for direct applications in an attempt to create an incentive for customers.

Borrowers who apply directly to obtain this lower rate also lose access to a broad lender panel, where cheaper options may exist.

Transparency and Protection

Transparency is a requirement for all licensed brokers.

Credit Proposal Disclosure documents that outline exactly what they earn are mandatory before you proceed.

Unlike bank staff, brokers are also legally required to act in your best interests.

Exceptions: When a Broker Might Charge You

While most consumer mortgage brokers are free to the borrower, there are some scenarios where fees may be payable by the borrower.

Common scenarios where you might encounter a fee include:

- Pre-Approval Fee: A fee for service that is refunded on settlement of the loan.

- Small Loan Amounts: For loans typically under $250,000, the standard bank commission often does not cover the cost of processing the application.

- Fee-for-Service: A transparent model where the broker charges a flat engagement fee to remove bias, then rebates the lender commission back to you.

Where fees are much more common are in commercial mortgage lending.

These loans can require a much larger time commitment for a broker and the lending timeframe can also be shorter.

This limits the commission opportunity for the broker and fees are intended to offset this.

Some examples include:

- Commercial Loans: Often required for development project of three dwellings or more, or the purchase of multi-unit residential buildings.

- Complex Ownership Structures: SMSF lending, and trust structures involve significantly more administrative and legal work than standard residential mortgages.

- Non-Standard Income: “Low-doc” loans for self-employed borrowers often require extensive verification work that justifies a service fee.

Before Paying Any Fees

Any fee must be disclosed upfront in a document called a Credit Quote.

This is a legal compliance requirement.

Never agree to a fee without written documentation detailing the exact scope of work, when payment is due, and refund terms if the loan fails to proceed.

If a broker demands a fee just for an initial chat or assessment, consider walking away.

Gusto Home Loans do not charge any upfront fees on standard residential mortgages, so get in touch today for an obligation free consultation.

Can a Broker Charge You a Clawback Fee?

A clawback occurs when a lender reclaims the commission paid to a broker because the loan was refinanced or discharged early.

Typically within 12 to 24 months.

This is a commercial agreement between the lender and the broker. It is not a debt that you owe.

In the past, some brokers may attempt to pass this loss to the borrower by enforcing a clawback recovery fee.

This practice is no longer allowed under Australian regulations and you are not liable for any lost commission by the broker.

Frequently Asked Questions

Do I pay a mortgage broker for a first home loan?

For a standard residential home loan, the answer is usually no. The lender pays the broker a commission when the loan settles, which covers their service. All payments will be documented within the Credit Quote provided to you.

Does it cost money to talk to a mortgage broker?

A discovery call or initial consultation is typically free. Most brokers operate on a success-based model where they only get paid if your loan settles.

If I don’t proceed, or I’m not approved, do I owe the broker money?

Under a standard commission model, you generally pay nothing if the loan does not settle. Some brokers may request an upfront fee for a pre-approval that is refunded on settlement, but this is not the norm.

Summary

Most borrowers never pay a mortgage broker directly.

The lender typically pays the commission upon settlement and all payments are disclosed in the compliance documents provided.

Gusto is built on fee transparency and high-support service. Whether you are buying your first home or refinancing an investment, speak with us for a clear comparison of your lender options and borrowing power.