While you cannot withdraw your superannuation to use as a deposit on your first home, you can leverage the First Home Super Saver (FHSS) scheme to get there faster.

This tax-effective strategy bridges the deposit gap faster, mismanaging the strict release timelines often leads to contract breaches.

We explain how to navigate FHSS rules, align settlement dates, and combine these funds with 5% deposit options to secure your home without costly errors.

What is the First Home Super Saver (FHSS) Scheme?

The FHSS scheme allows first home buyers to save voluntary contributions inside super, then release the eligible amounts (plus deemed earnings) for a deposit.

You cannot withdraw the compulsory super contributions paid by your employer.

That part of your super balance remains protected until you reach retirement age.

Why Use the FHSS?

The scheme allows you to improve your tax position on money you will need to save anyway to raise a house deposit.

Concessional contributions are taxed at 15% rather than your marginal income tax rate (which can be up to 45% + the 2% medicare levy).

You also get a tax discount of 30% on withdrawal of the funds in preparation for your home purchase.

This allows you to build a deposit much faster than saving from your take-home pay that is taxed at a much higher rate.

It is essentially free money from the government if you are eligible.

Scheme Rules and Limitations

You can only access the extra funds contributed via salary sacrifice in addition to the mandatory contributions.

There are some limitations to the scheme that should be considered prior to making additional contributions:

- Annual Cap: Up to $15,000 of voluntary contributions counts per financial year.

- Release Cap: Maximum $50,000 in contributions across all years per person.

- Couples: Partners can combine caps to potentially release $100,000.

These limits sound low relative to the size of a deposit needed for the median house in Australia.

But when combined with the First Home Buyer Guarantee scheme (that only requires a 5% deposit), you can see why this is a springboard to faster home ownership.

A $50,000 deposit can secure a property up to $1 million, assuming you can also support a mortgage of $950,000.

To raise that $50,000 there are some additional rules around the balance available for withdrawal to consider:

- 100% of your eligible personal voluntary contributions you haven’t claimed a tax deduction for (non-concessional contributions)

- 85% of your eligible salary sacrifice contributions (concessional contributions)

- 85% of eligible personal voluntary super contributions you have claimed a tax deduction for (concessional contributions)

Read the full rules of the scheme here.

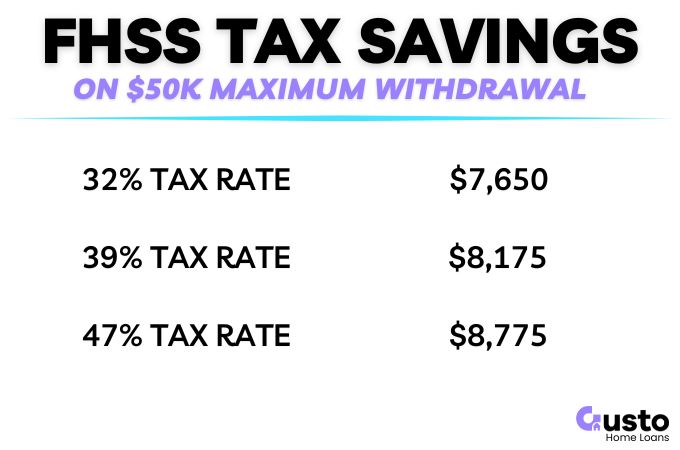

How Much Tax Can I Save?

The benefits of the scheme will vary depending on your marginal tax rate.

If withdrawing the maximum $50,000 contribution your approximate tax savings are below.

This is an example only and there may be variations in your personal circumstances.

Especially if your marginal tax rate changes throughout the participation period.

| TAX RATE + MEDICARE LEVY | 32% | 39% | 47% |

|---|---|---|---|

| Income Tax Savings (15%) | $16,000 | $19,500 | $23,500 |

| Tax Paid on Super Contributions | -$7,500 | -$7,500 | -$7,500 |

| Tax on Withdrawals | -$850 | -$3,825 | -$7,225 |

| Net Tax Savings | $7,650 | $8,175 | $8,775 |

Downsides of the FHSS

The scheme is admin-heavy and strictly regulated.

You are not withdrawing your existing retirement savings, and your funds remain exposed to investment market volatility.

So you could make a loss after all this work if your Super investments perform poorly.

FHSS release times also vary, and your contract finance date must align with the withdrawal process to ensure a smooth transaction.

If you are targeting a specific purchase window, talk to our team of brokers early to ensure that all things line up.

Who Is Eligible for the FHSS Scheme?

To qualify, you must be 18 years or older and have never owned property in Australia, including investment properties or commercial premises.

You must buy a dwelling that is intended to be used as your principal place of residence and must live in the property for at least 6 months within the first 12 months of purchase.

What if my Partner has Owned Property?

Many buyers assume that if their partner has owned property before, they are both ineligible. While this is the case for a number of first home buyer schemes, FHSS eligibility is assessed on an individual basis.

If you are a first-home buyer but your partner is not:

- You can generally still use the FHSS scheme for your portion of the deposit.

- Your partner cannot access the scheme.

- You must confirm your specific ownership structure matches ATO requirements.

Can I Purchase Vacant Land?

You cannot use released FHSS funds to simply buy and hold a vacant block of land.

To satisfy release requirements, you must enter into a contract to construct a home within 12 months of the release request.

The home must then also be your principal residence.

FHSS Release Application Checklist

Timing is critical with a property contract that also relies on a government run scheme.

A miscalculation, or delay, and your deposit funds could be inaccessible at settlement.

Follow this sequence to ensure your funds are ready:

- Step A: Check myGov to confirm your voluntary contributions are classified correctly.

- Step B: Request an FHSS determination via ATO online services.

- Step C: Once you have a determination, request the release. Ensure it includes the total amount.

- Step D: Allow 15–20 business days for the ATO to release funds. Do not assume instant transfer.

- Step E: Sign Contract. Rules changed on 15 September 2024 allowing determinations after signing (if no release requested), but getting it early remains the safest approach.

Signing at the wrong time can mean your FHSS money is locked out of that purchase, forcing you to proceed without it, or triggering additional tax liabilities.

You can better protect yourself from administrative hiccups by negotiating a longer settlement, or finance clause, that accounts for the 20-day ATO release window.

Can I Just Withdraw My Super to Buy My 1st Home?

You can only release your super to buy a house if you have reached the eligible retirement age.

That is a long wait to buy your first property!

The FHSS scheme is a tool that allows you to leverage the Super tax benefits and the managed investments within your fund to accelerate your pathway to home ownership.

It is not a back channel that allows you to release extra money intended for your retirement.

Frequently Asked Questions

Can I use my employer super contributions for FHSS?

No. You can only release voluntary contributions you have personally made, such as salary sacrifice or after-tax transfers. Mandatory employer Super Guarantee (SG) contributions are not eligible for withdrawal.

Can I release FHSS funds if I already signed a contract?

You must act immediately. While recent rule changes provide some flexibility regarding determination dates, the release request window remains strict. Check your determination status instantly and speak to your conveyancer.

If my partner owned a property before, can I still use FHSS?

Yes. FHSS eligibility is assessed on an individual basis. Even if your partner is ineligible due to prior property ownership, you can still use the scheme for your portion of the deposit.

How long does FHSS release take?

The ATO advises a standard processing time of approximately 15 to 25 business days. Do not commit to a deposit due date on your contract that assumes an instant payment from your super fund.

Can I use FHSS with the First Home Guarantee?

Yes. These are separate government initiatives that can be combined. You can use the funds released via FHSS to satisfy the 5% genuine savings requirement for the First Home Guarantee.

Summary

The FHSS is a big leg up for your savings goals and when combined with the First Home Buyer guarantee scheme can get you into a home much sooner.

Superannuation has long been a tax advantaged vehicle that benefits older Australians far more than the younger generations.

By accessing the benefits of the FHSS you can get back some of those tax dollars and direct in towards that first home purchase.

Need some help navigating the various first home buyer support schemes? Get in touch with our team of experts today.

They will be able to help you navigate the eligibility criteria, and formulate a plan and pre-approval for what you can afford.