Building up a large balance in your mortgage offset account can be tricky when you have your regular expenses being managed from the same place.

The balance just never seems to go up, and there is always another expense just around the corner.

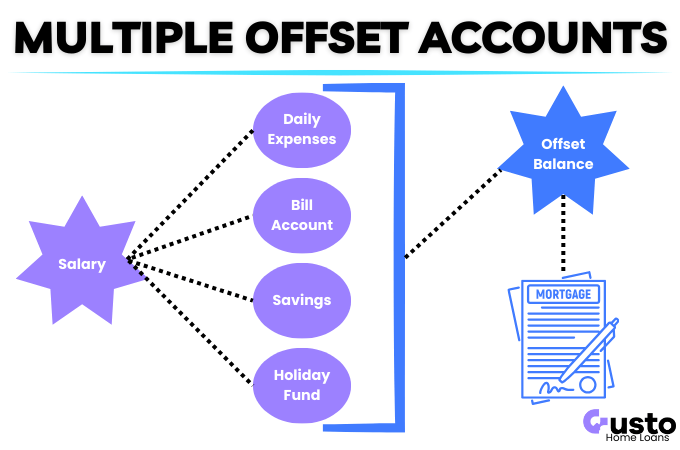

Some lenders have realised this and allow you to create multiple offset accounts so you can manage your money in a more organised way.

You can have a transaction account, dedicated bill paying account, and savings all linked to the one home loan.

Each one of them reduces the daily interest on your mortgage.

In this article, we’ll discuss the benefits of having multiple offset account and how to organise them for maximum benefit.

How the Multiple Offset Bucket System Works

Instead of pooling cash into one confusing pile, you can create a dedicated buckets (accounts) for specific purposes.

Some common examples may include the following, but they can be whatever is most relevant to your situation:

- Everyday spending offset

- Bills and quarterly expenses offset

- Emergency fund offset

- Holiday or renovation offset

The lenders aggregate the balances in each of the linked offset accounts when calculating daily interest.

Every dollar across these buckets still reduces the overall balance of the mortgage, reducing the interest you pay.

This becomes easy to manage because you can set up automatic transfers to allocate fixed amounts to each bucket.

No manual money management required.

The big caveat to this is that not all lenders provide the option for multiple accounts. So you must be with a compatible lender to implement this setup.

To discuss your home loan options and optimal offset account setup get in touch with our expert team below.

Maximise Interest Savings Across Multiple Accounts

Many borrowers worry that splitting cash across several accounts dilutes their interest savings. This is a misconception.

If you have a $500,000 mortgage and $50,000 spread across multiple offsets, the lender only charges daily interest on $450,000.

Dividing your money into different buckets does not reduce the financial benefit.

The real advantage is making it easier to keep more cash offsetting your home loan.

You can naturally increase your average balance with two simple tactics:

- Direct your salary into an offset account so your balance peaks on payday.

- Leave short-term savings in these accounts until the exact day you need the funds.

- You could also use credit cards for your daily expenses and pay the balance at the end of each month (interest free).

Always check with your lender to confirm every linked account provides a 100% full offset, as some products only offer partial offsets on secondary accounts.

Protecting Cash With Multiple Offset Accounts

Locking your savings into extra loan repayments leaves you cash-poor when life happens.

Offset accounts reduce your interest exactly like extra repayments do, but your money remains completely accessible.

Multiple offset accounts strengthen this safety net by physically separating your funds.

You can quarantine money for large planned expenses, including:

- Car replacements

- School fees

- Annual council rates

When an unexpected expense hits, you simply draw from these offset funds instead of relying on expensive credit cards or personal loans to make up the difference.

For a practical safeguard, keep your emergency bucket separate from your everyday spending account.

Set a minimum balance floor that you never drop below to remove the temptation to spend.

While multiple accounts build financial discipline, opening too many creates unnecessary admin.

Choose the minimum number of accounts that works for you.

Managing Joint and Individual Offsets

Merging finances often creates friction when spending styles differ. The goal is mortgage transparency without arguing over personal purchases.

With one mortgage and two incomes, do you need joint offsets, individual accounts, or both? Consider these structures:

- All-joint: Salaries fund shared bills, everyday spending, and emergency offsets for maximum simplicity.

- Hybrid: Share joint bills and emergency accounts, but maintain two personal spending offsets for relationship harmony.

- Mostly-individual: Maintain individual offset accounts and contribute a set amount to one shared bills offset.

As long as accounts are officially linked to your loan, the combined balances reduce your interest charges.

Some guardrails that help you stick to your plan can include:

- Automating your funds transfers on payday.

- Keep statement visibility and account access clear for both borrowers.

- Calculate shared expenses and the required contribution so there are no surprises.

The Cost of Multiple Offsets

Multiple offset accounts are usually bundled into package home loans that carry annual account keeping fees or slightly higher interest rates.

A simple break-even calculation ensures the setup is worthwhile.

First, identify your total annual package fees.

Next, estimate the annual interest saved from your average offset balance.

If projected savings comfortably exceed those fees, the strategy makes financial sense.

These savings multiply with a higher average balance, higher interest rates, and a longer holding timeframe.

Conversely, the benefit disappears if you only hold a few thousand dollars.

High fees, inconsistent contributions, and unused buckets will also reduce your net savings.

Frequently Asked Questions

How many mortgage offset accounts should I have?

You may only need one if you are disciplined in your spending. Two may help you separate savings and regular expenses. Any additional offsets should have a specific purpose or it just creates work.

Do multiple offset accounts reduce interest more?

No, there is no additional savings from having multiple offset accounts. It is the aggregate balance that is used to calculate the interest savings. Using additional accounts can improve your budgeting behaviour rather than delivering extra financial benefits.

Do offset accounts cost extra?

Often, yes. Lenders package them into loans with annual account keeping fees or higher interest rates. You should consider the full offering from the lender rather than looking at this cost in isolation.

Summary

Multiple offsets help you organise money into buckets, keep more cash offsetting daily, and stay liquid for emergencies.

It also makes it easy to develop financial discipline over time as you pay down your mortgage.

Always be mindful of an associated costs.

Things like annual package fees can wipe out these interest savings if your offset does not have a sufficient balance in it.

Unsure which lenders support your ideal structure? Our brokers will compare options and confirm exact offset rules before you apply.