Minimising mortgage interest requires balancing significant savings with immediate access to cash.

While offset accounts and redraw facilities both reduce your interest bill, they behave differently regarding daily access, fees, and tax outcomes.

Comparing Redraw vs Offset comes down to your cashflow, future investing plans, and risk tolerance.

This plain English comparison highlights the right choice for first home buyers, upgraders, and investors to avoid costly tax mistakes.

First, a quick primer on how each works.

How Redraw and Offset Accounts Work

These tools are generally offered with variable interest rate mortgage products.

While you could also access them with a split loan, fixed rate home loans are much more rigid around interest saving features.

Offset Account

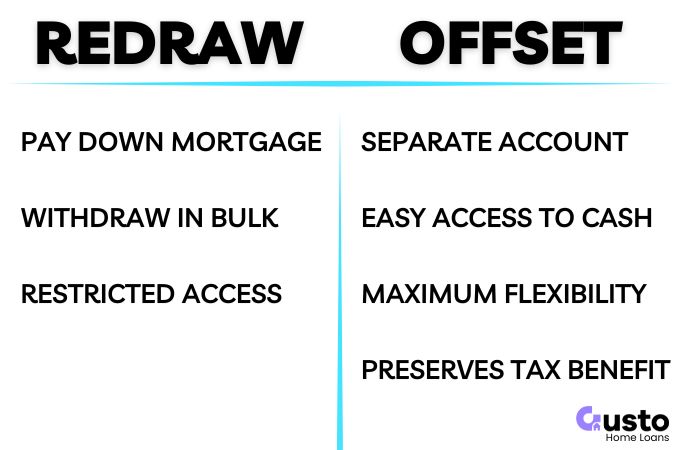

An offset account is a transaction account linked to your mortgage.

The lender calculates your interest on your loan balance minus your offset balance, which reduces your interest costs.

The funds are never paid into your mortgage which has two advantages:

- You retain access to the funds at any time.

- You preserve any current or future tax deductibility of the interest expenses that you may be entitled to.

Some lenders also offer multiple offset accounts linked to the one home loan.

This allows you to set up a good budgeting system that will maximise the reduction in interest costs.

Redraw Facility

A redraw facility is a loan feature allowing you to withdraw extra repayments made above your minimum schedule.

You are paying down the principal and then drawing down on that balance again.

Some implications of this setup are:

- Access to the funds can have restrictions around it (e.g. minimum redraw amounts).

- Drawing down funds can complicate tax deductibility of any interest costs, depending on what you do with the funds after it is redrawn.

The tax considerations are generally irrelevant for those living in their principal residence and just trying to pay it down as quickly as possible.

However, plans change in the future and if you need to rent the property out there will be implications to consider.

Redraw vs Offset : Detailed Comparison

1. Interest Cost Savings

Both tools support the same objective of reducing the daily balance used to calculate your mortgage interest.

The difference is in the separation of funds, not the net savings.

With an offset account, interest is charged on your loan minus your savings.

For example, a $500,000 loan with a $50,000 offset means paying interest on $450,000.

Your savings depend on how long that cash stays parked in the offset.

Extra repayments into a redraw facility achieve the same outcome by directly reducing your loan principal.

Interest drops because your actual debt is lower.

The real difference emerges when money moves.

If you constantly pay daily expenses from an offset, your average balance drops, diluting your savings.

Ultimately, the best tool is whichever helps you maintain the highest consistent balance over time.

2. Accessibility and Lender Control

The clearest difference is accessibility of the additional funds.

Choosing the feature that matches your intended use will achieve the best outcome.

An offset account behaves much like an everyday transaction account.

You can:

- Deposit your salary

- Pay routine bills

- Use a linked debit card

This instant access makes an offset ideal for holding emergency funds and managing irregular expenses.

A redraw facility lets you withdraw extra repayments under strict lender rules.

Access often involves minimum withdrawal limits, processing windows, and policy changes.

Lenders also periodically recalculate your available redraw, meaning the number you see today might not be what you can access tomorrow.

Especially when interest rates are on the way up.

This controlled environment suits disciplined borrowers who prefer to pay down debt and leave it alone.

3. Cost of Offset vs Redraw

Offset accounts usually require loan packages with annual fees or slightly higher interest rates.

Conversely, redraw facilities are often free on basic home loans.

A small offset balance combined with high fees is poor value.

For example, with a $395 annual fee and a 6% interest rate, you need around $6,500 sitting in your offset all year just to break even.

Multiple offset accounts are excellent for household budgeting.

However, lenders may restrict how many you can open or require a premium product to access them.

Before deciding, the Gusto team will always confirm the following:

- Annual package fees

- The interest rate difference

- Redraw limits and access fees

- Number of offsets allowed

4. Current and Future Tax Risks

When choosing between a redraw and an offset, the deciding factor is often the tax implications of each facility.

The ATO generally treats a redraw as a new borrowing event. Tax deductibility depends entirely on how you spend those funds.

Redrawing money for a holiday and later for shares creates a mixed-purpose loan.

This guarantees an apportionment and record-keeping nightmare at tax time.

Conversely, withdrawing from an offset account is simply spending your own cash. It never taints the original loan purpose.

If you plan to upgrade your home and rent it out later, your loan structure matters.

Always confirm investment deductibility with an accountant to maintain clean records and maximise tax benefits.

5. Risks and Reliability

An available redraw balance in your banking app does not guarantee immediate access to those funds.

A redraw is not a savings account. It simply lets you withdraw extra repayments you have made.

Because access depends on lender policy, your app only provides a guide. Your actual entitlement will be specified in your loan contract.

Review your mortgage terms for these common restrictions:

- Withdrawal notice periods

- Minimum retained balance limits

- Access blocks during fixed-rate periods

- Account freezes triggered by hardship or arrears

In contrast, an offset account sits in your name and offers direct control over your money.

If you need guaranteed emergency liquidity, do not rely solely on a redraw facility.

6. Financial Discipline

Offset balances often feel like spendable money.

If you are a first-home buyer struggling to keep savings untouched, redraw creates an out of sight, out of mind barrier to enforce budget discipline.

This is where an honest self assessment can be helpful so you can get ahead over time.

Whereas someone planning a future investment may need the flexible cash buffer an offset account provides.

They park all their extra funds in the offset and can access any time for a deposit on an investment property.

While also preserving the tax deductibility of the interest on the first mortgage.

7. Future Borrowing Power

Another consideration is how your total debt is calculated in the eyes of a future lender.

If you have paid down the principal on your mortgage then your total debt is lower, until you choose to redraw funds.

Whereas money in an offset does not reduce your total debt levels.

This can be important when considering your debt to income ratio and other potential limitations in your finances.

Before applying, ask your broker exactly how your cash buffer will be treated in serviceability assessments.

Which Feature is Best for You?

An offset account is the safest all-round option that maximises flexibility and protects any changes in your future plans.

Assuming that the savings will outweigh any costs of maintaining the facility.

However, this will vary depending on the type of borrower and their individual objectives.

Some examples include:

First Home Buyers

May prioritise the need to build up a cash buffer early on while debt levels are high.

- Choose an offset account to maximise interest savings from salary deposits, and to retain access to cash for emergency purposes.

- Opt for a redraw facility if you need forced savings discipline and zero ongoing fees.

Upgraders

If earning capacity is strong, and paying off your mortgage is the priority, then an offset account may have no useful purpose.

A redraw may be more suitable as a back up if funds are ever required for an emergency, or to fund future investments.

However, if there is a chance your current home might become an investment property at any point in the future then an offset account will preserve the original loan balance.

This is critical to maximise the tax deductibility of the interest payments.

Property Investors

Would generally use an offset account for maximum cashflow flexibility and to preserve tax deductibility of the original mortgage.

Frequently Asked Questions

Can you have both offset and redraw on the same loan?

Yes, many variable rate mortgages allow you to use both features simultaneously.

Is offset available on fixed loans?

Lenders typically restrict offsets on fixed rates. You can solve this by splitting your loan to keep a variable portion open.

What should I ask my lender or broker before choosing an offset or redraw?

Request a break-even calculation for how much is needed in the offset account to save more than the cost of the facility. You must also verify limits regarding minimum redraw amounts and the number of allowed offset accounts.

Should I Use a Redraw or Offset Account?

An offset account offers the most flexibility and easiest access to cash, which can be a double edged sword.

If you are good at managing your household budget and accumulating savings then the offset can be the best of both worlds.

Your net debt is lower, but you can also turn your home into an investment property at any time without losing any of the tax benefits.

If you just want to be debt free as soon as possible, with no plans to move, then a redraw option may be cheaper and more suitable.

To discuss your home loan options and what features might be best for you, get in touch with our expert team below.