Most diligent home owners and investors are always on the lookout for a better deal on their mortgage.

And rightly so! Even a small reduction in your interest rate can mean thousands of dollars in savings over the life of your loan.

However, if you have committed to a fixed interest rate period, then refinancing is not going to be as straight forward when compared to a variable rate mortgage.

In this article, we will discuss the financial implications of refinancing a fixed rate loan and how to navigate what could become a costly exercise if managed incorrectly.

Why Refinancing a Fixed Rate Home Loan is Different

People usually fix their interest rate so they have certainty in their repayment obligations and are not subject to the whims of the economy and the RBA for the fixed rate period.

What some may not consider, is the lender also relies on that predictability of outcome when funding the loan.

Repayment Certainty Comes with Obligation

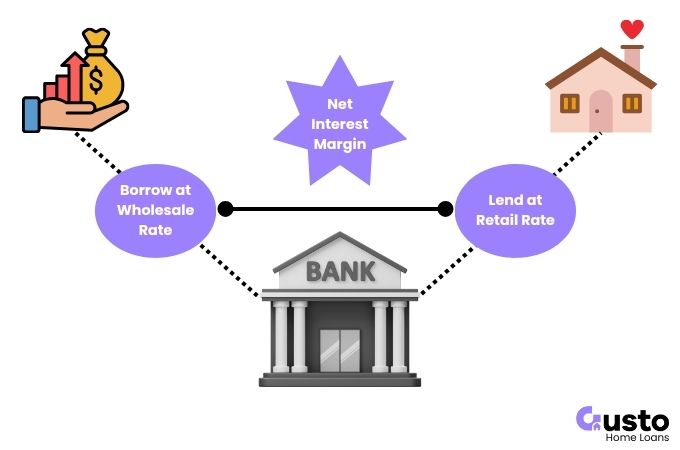

A lender will fund a fixed rate mortgage from sources that will also be at fixed rates.

The margin between their cost of borrowing and the income created by lending to you is how they make their money.

Also known as the Net Interest Margin (NIM).

If you decide to refinance before the fixed period ends, and market interest rates have fallen, then the lender will not be able to achieve the same return on those borrowed funds and will lose money.

So the question is, who is liable for that lost income?

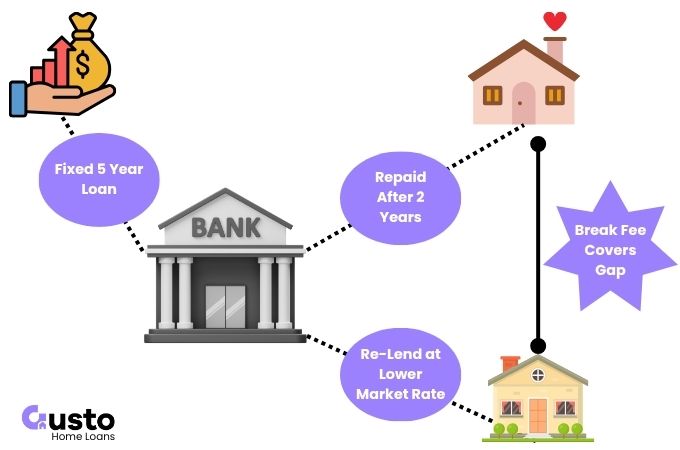

Refinancing Breaks the Contract

By refinancing within the fixed term, you’re effectively terminating your contract ahead of the agreed repayment schedule.

Given that this action is initiated by you, you will also be obliged to cover the lender’s potential losses.

These are known as break fees.

The amount you pay will depend on the amount of time remaining in your fixed term, and the difference between the wholesale rate at the time of funding and the current rate.

How Break Fees Are Calculated

The break fees are a calculation of how much future income the lender would lose over the remainder of the fixed rate period.

Where this gets tricky is the interest rate differentials are calculated on the lender’s wholesale borrowing rate, and not the customer’s retail rate.

The basic formula is as follows:

Break Cost = Loan amount prepaid * (Interest Rate Differential) * Remaining Term

This will be much easier to understand with an example.

Let’s assume the following:

- $500,000 mortgage with a fixed interest period of 5 years.

- Interest only repayments for the fixed rate period.

- The interest rate was fixed in Nov-23 at the peak of the latest interest rate cycle and the bank’s wholesale rate at the time was 4.55%.

- Rates have declined by 0.75% in the two years since the mortgage was opened, leaving three years remaining in the fixed term.

If we plug these numbers into our formula we get a break cost of $11,250.

$11,250 break cost = $500,000 loan amount * (0.75% – interest rate differential) * 3 years remaining

A break fee of this size is enough to turn many people off refinancing while still within the fixed rate period.

However, the cost is only half the story. What about the benefit you can capture by doing so?

Calculating the Benefit of Breaking Your Fixed Term

The benefits of breaking your fixed term mortgage and moving to a new lender must exceed the cost of doing so by enough for the time investment to be worthwhile.

If the alternative interest rate was 0.75% lower than your fixed rate then the cost comparison is neutral, and you would not bother doing so.

However, there are multiple factors in your favour:

- The retail mortgage market can shift much more than any change in the RBA cash rate due to competitive pressures and expectations of future rate cuts.

- You pay the break fee on the wholesale interest rate the bank incurs, but you calculate the benefit to you based on the retail rate.

If the market conditions are right then you can take full advantage of this and secure a much lower interest rate and save thousands over the life of the loan.

If we look at the current mortgage market there is a huge opportunity for people to save big that may have fixed their rate at the peak of the market.

Let’s consider two refinance options.

Refinance to a Fixed Rate

Our break even target is an improvement of 0.75% so that the break fee is worth paying.

Where things can get more complicated is if you reset your loan term to 30 years, which will increase the lifetime cost of the loan.

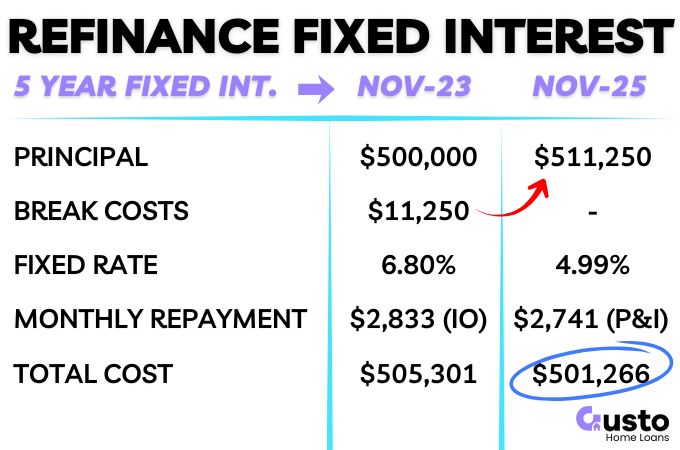

If we look at historical fixed rates we can see that at the peak the average 3 year fixed rate was 6.8% in Nov-23.

We will use this rate for the purpose of the example.

As of Nov-25 there are fixed rates available from 4.99%.

That is a 1.81% reduction in the rate! A huge potential saving!

This will allow you to move to principal & interest (PI) repayments while also lowering your repayments.

Note: If you prefer to stick with interest only then your repayments will be much lower but your life of loan savings may evaporate. So it depends on your overall strategy what you choose to do.

Let’s look at the numbers:

- Existing $500,000 loan:

- $2,833.33 IO monthly repayments (assumes a 6.8% fixed interest rate).

- $3,011.01 PI monthly repayments after fixed rate/IO period expires (5.3% variable rate).

- $505,301.79 remaining cost.

- Refinance to a $511,250 loan (break costs included):

- $2,741.38 (PI) monthly repayments (assumes 4.99% fixed interest rate).

- $501,266.37 remaining cost (5.3% variable rate after fixed term).

Despite the chunky fee, AND moving to principal and interest repayments, AND extending the repayment period by an extra two years, both the repayment and total cost have reduced compared to staying in the current loan.

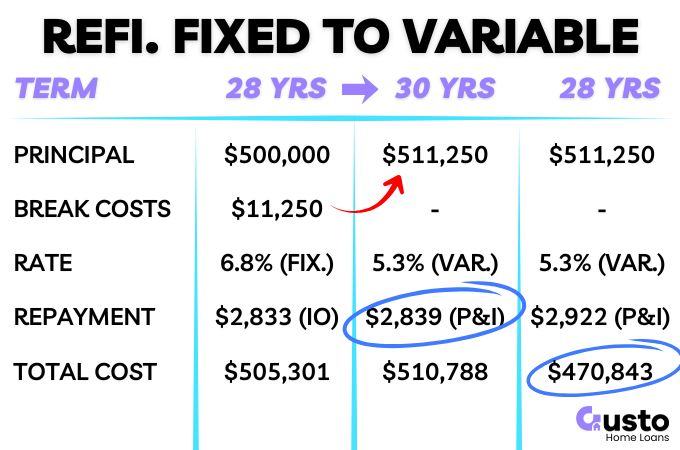

Refinance to a Variable Rate

Using the same scenario and refinancing to the 5.3% variable rate from day one, we get the following figures.

- Refinance to a $511,250 loan over 30 years (break costs included):

- $2,839.00 (PI) monthly repayments.

- $510,788.00 remaining cost.

The repayments have only increased by $6 a month and you are now paying Principal and Interest.

In three years time your repayments will be $172.01 a month lower than if you stayed in your current loan.

However, the lifetime cost has increased by around $5,000. So the primary benefit is the reduction in repayments and accelerated path to building equity.

If the term of the new loan is 28 years, to match the remaining term of the current loan then you can save big on the lifetime cost:

- Refinance to a $511,250 loan over 28 years (break costs included):

- $2,922.00 (PI) monthly repayments.

- $470,843.00 remaining cost.

In this scenario you will save a massive $34,458.79 over the life of the loan!

If interest rates continue to fall then your savings will also increase.

Not yet sure if it makes sense for you to refinance? Get in touch with our home loan exports today and we can help calculate the benefits for you.

When It Makes Sense to Refinance a Fixed Rate Loan

It makes sense to refinance your fixed rate loan when there is an overall financial benefit to doing so, if the repayments will be more manageable, or for other lifestyle reasons.

Current Mortgage Rates Are Favourable

We have shown in the previous examples, there are multiple ways to structure your refinance to maximise the benefit to you.

And the savings can be in the tens of thousands of dollars!

These opportunities are more likely to be available in a falling interest rate environment, or when there is a surge of competition amongst mortgage lenders.

You Expect Future Interest Rate Cuts

The break fee calculation is done using the rates on the day of your final settlement.

If conditions indicate there will be future interest rate falls and you can refinance before they take place then you could minimise your break fees and move to a variable rate.

You will then gain maximum benefit from any future rate cuts.

However, interest rate predictions do not always play out. So there is risk associated with this approach due to the reliance on market forces (aka luck).

No Other Option to Access Equity or Consolidate Debt

In most cases you would be better off applying for a top up loan with the same lender to access additional equity.

Only when your current lender cannot accommodate your requirements should you consider refinancing the fixed rate loan elsewhere.

For example, banks are required by APRA to assess your loan serviceability using the actual interest rate plus a 3% buffer.

Non-banks do not have this requirement and may allow you to borrow a much higher amount.

While it will be expensive to refinance, the overall benefit may be worth it to you if you can pay off other high interest debt, accelerate renovations to your home, or just for lifestyle reasons you can comfortably afford.

When You Might Want to Hold Off Refinancing

While it can be frustrating to pay a higher interest rate than the current market would dictate, sometimes it is the best financial move to just tough it out and learn from the experience.

Refinancing too soon can be an expensive mistake.

Your Fixed Period Is About to End

If your fixed interest period is coming to an end then you may be able to avoid break fees altogether if you time your refinance well.

You can use the time leading up to this deadline to prepare your refinance application so that you can switch to a better deal as quickly as possible while avoiding the additional fees.

If Your Break Costs Are Too High

Sometimes, the penalty will be far too high. It is not uncommon to see break costs that are well over $10,000!

If your estimated savings are lower than the total break fee and refinancing costs, then staying put until your fixed term ends would be the wiser choice.

Insufficient Equity to Capitalise Break Fee

Unless you prefer to pay your break fee in cash (almost no one ever does!), then you need enough equity to pay out your current loan, add the break fee, and still be under an 80% loan to value ratio.

If you go above this then you may be liable for lenders mortgage insurance which could blow the cost savings out of the water.

This is why it is important to know your numbers inside out before initiating the refinance.

If You’re Planning to Sell Your Property

The benefits of refinancing are only realised over the long term.

It rarely makes sense to move your mortgage to another lender if you are going to hold the asset for less than 12 months.

The numbers just won’t stack up.

Can Break Costs Ever Be Negotiated or Waived?

A lender may waive break fees in very specific circumstances. Significant financial hardship or a special retention offer may be the only scenarios that it would be possible.

However, for a straight refinance to another lender your chances are zero.

Other Fees to Expect

In addition to the break costs you may also incur a discharge fee and some administrative fees to settle the loan.

As part of the refinance you will also incur some fees to set up your new loan. Which can include a valuation fee, establishment fee, and settlement fees.

These all vary depending on your loan agreements and have not been included in the earlier examples.

Calculating your switching costs is a critical part of the decision to refinance at all, and this is where a good mortgage broker can help so you know the full picture before initiating the application.

Click below to get in touch with our expert team so you have the full picture prior to refinancing your loan.

Conclusion

In most cases you can capitalise your break fees when refinancing your home loan within the fixed rate period.

So your new loan will start with a slightly higher balance, but over time the savings will compound.

As seen in the example calculations, if you do not extend the loan term back to 30 years then your savings are amplified significantly.

If you can spend $11,250 to save over $30,000 then that is a sound decision that will only benefit you over the long term.