Stamp duty can add tens of thousands of dollars to the upfront costs of buying a property.

However, first home buyers have access to exemptions in most states to reduce this burden when entering the property market.

Government concessions can potentially reduce this tax to zero, but strict eligibility criteria apply.

And in some cases your target property may not be eligible at all.

In this article, we’ll give you the state-by-state run down of the first home buyer assistance schemes and how to qualify.

Understanding Stamp Duty and Transfer Costs

Stamp duty (or transfer duty) is a state government tax on transferring property ownership.

Outside of your deposit, it is usually the single largest upfront cost you will face.

Unlike your deposit, which contributes to the purchase price, stamp duty is an additional transaction cost usually payable at or before settlement.

The amount you pay is calculated on the dutiable value.

This is the contract price or the market value, whichever is higher.

If a family member gifts you a property, you are still taxed on its full market value.

Beyond value, two key factors drive the calculation:

- Property Type: Rates and rules differ significantly between established homes, new builds, and vacant land.

- Buyer Intent: Owner-occupiers can sometimes access concessions that investors cannot.

First Home Buyer Exemptions

As a first home buyer, your assessment will result in one of three outcomes:

- Full Exemption: You pay $0. This applies when the property value is under your state’s exemption threshold.

- Concession: You pay a reduced amount. This applies on a sliding scale when the value is slightly over the exemption limit but under the price cap.

- Full Duty: You pay standard rates. This happens if the price exceeds the concession cap or you fail a residency test.

While the concepts are simple, there are some eligibility rules regarding contract dates and residency can disqualify you instantly.

For a quick eligibility check you can get in touch with our expert team below. They can run a check as part of a preliminary assessment of your home loan options.

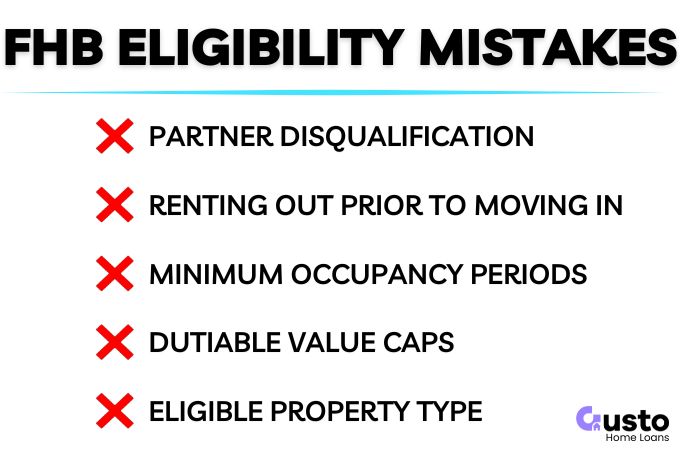

FHB Exemption Eligibility Traps

Miss a deadline or misinterpret a residency clause, and the Revenue Office will issue a reassessment notice for the full amount of duty, plus interest.

To keep your concession, you must navigate these specific eligibility pillars.

Spouse and Partner Disqualification

In most jurisdictions, if your spouse or de facto partner has owned residential property in Australia before, you are both disqualified.

This applies even if they are not listed on the title for the new home.

Only QLD decides stamp duty liability by the portion of your share in the home you are purchasing.

Allowing you to claim an exemption if your partner has previously owned a property.

Rentvesting and Occupancy

Concessions are strictly for owner-occupiers. You must generally move in within 12 months and reside there for a continuous period (usually 6–12 months).

If you lease the property immediately, you lose the concession.

The only safe path is to complete your occupancy period first, then rent it out.

If you vacate before your continuous residency period ends, you are legally required to notify the revenue office.

You will then be reassessed to pay back the duty saved, plus potential penalties if there is a clawback.

Off-the-Plan Concessions

In most states there are price caps on the price of the property to be eligible for a full or partial discount.

If you are purchasing something new that is above one of the caps, double check how the dutiable value is calculated.

There may be allowance where the duty for off-the-plan purchases are calculated on the dutiable value (land value) rather than the full contract price.

Property Type

You may only qualify for an exemption when buying a new dwelling in some states.

For example, if you are planning to buy an existing house in South Australia you are not going to be eligible for an exemption at all.

So you are going to have to factor the cost of stamp duty into your funds required to complete the transaction.

State-by-State Stamp Duty Exemptions

Dutiable Value Price Caps

Every state has a different exemption threshold for the maximum value of the property being purchased.

The numbers below are correct for the duration of FY26, but they are adjusted over time.

In some states the limits are quite low in relation to the median house price. However, most first home buyers will be purchasing well below the median.

| State | Full Exemption | Partial Exemption | Full Exemption (Vacant Land) | Partial Exemption (Vacant Land) |

|---|---|---|---|---|

| NSW | $800,000 | $800,000 to $1,000,000 | $350,000 | $350,000 to $450,000 |

| VIC | $600,000 | $600,000 to $750,000 | $600,000 | $600,000 to $750,000 |

| QLD | $800,000 | NA | $800,000 | NA |

| WA | $750,000 to $1,000,000 | NA | $350,000 | $350,000 to $450,000 |

| SA | No Cap (New Homes Only) | NA | No Cap | NA |

| TAS | $750,000 | NA | $750,000 | NA |

| ACT | $1,020,000 | $1,020,000 to $1,455,000 | $1,020,000 | $1,020,000 to $1,455,000 |

| NT | No Cap (New Homes Only) | NA | No Cap | NA |

New South Wales (NSW)

The NSW scheme has frustratingly low price caps for first home buyers.

Even in fringe suburbs that are 90 minutes from the CBD the median price can be upwards of $1 million.

This makes it challenging for a FHB to buy a standalone house under the cap.

But there are plenty of apartments eligible for the full discount.

Neither you nor your spouse can have owned residential property in Australia previously to be eligible for the exemption.

You must move into the property within 12 months, and live there continuously for another 12 months.

Victoria (VIC)

Victoria has the lowest price cap on a full exemption, which is certainly true to form for the current government.

However, there are additional concessions available for off the plan purchases with the dutiable value reduced to be ex. construction costs.

This is only available until 21-Oct 2026 so you may need to move fast to take advantage of this program.

At least one buyer must satisfy the Principal Place of Residence (PPR) requirement and move in within 12 months.

Queensland (QLD)

QLD is the only state that allows you to claim an exemption based on individual ownership shares in the property.

So, if your partner is ineligible, you can still claim the concession on your share of the stamp duty liability.

This is a great option for couples who are buying together for the first time, but only one is a first home buyer.

You must also move in within one year to retain the benefit.

Western Australia (WA)

WA’s First Home Owner Rate of Duty provides $0 duty up to a set threshold and reduced rates up to a hard cap.

Limits vary by location with properties north of the 26th parallel of south latitude able to access a higher price threshold than those in Perth or Peel.

If you’re wondering what on earth this means, it is roughly in line with the northern border of South Australia.

South Australia (SA)

SA offers full stamp duty relief to eligible first home buyers building or buying a new home or vacant land.

Established homes are excluded and only new dwellings, or vacant land are eligible.

There are no price caps so there is no risk of exceeding a threshold for newly built house.

Occupancy rules are similar with 6 months required, starting within the first 12 months.

The only difference is for vacant land where the commencement must be either with 12 months from the completion of construction, or 36 months after settlement.

Tasmania (TAS)

Tasmania increased the duty discount from 50% to 100% in 2024, and has done a good job in revising the price caps to move with property prices.

While the current program is only confirmed until 30 June 2026, it may be extended and revised to a higher cap.

You must occupy the home for six continuous months and commence occupancy within the first 12 months to be eligible.

Australian Capital Territory (ACT)

The Home Buyer Concession Scheme reduces duty to $0 for properties within current value limits.

Which strangely are the highest caps in the country for a full exemption.

Partial concessions apply above this cap all the way up to $1,455m.

However, there are some additional conditions.

Unlike most states, eligibility relies on household income thresholds being below $250,000.

There are some additional allowances for the number of dependents you may have, but its not much.

This calculation includes your domestic partner’s income, even if they aren’t on the title.

The ACT uses a self-assessed system.

You must verify eligibility before claiming a concession code to avoid penalties for incorrect claims.

Northern Territory (NT)

Unlike other states, the NT has no permanent stamp duty concession for established homes.

Only new builds are eligible.

So if you plan on buying an existing dwelling you will need to pay the full rate.

Duty exemptions are only offered via the House and Land Package Exemption (HLPE) program.

A contract must also be signed before 30 June 2027 to be eligible.

You must buy from an eligible building contractor and move in as your principal place of residence.

How to Apply for a Stamp Duty Exemption

Every state will have their own set of application forms and submission channels.

Your conveyancer is usually responsible to submit the information and it will be up to you to ensure that takes place within the required deadlines.

This should be part of your initial discussions with both your conveyancer and mortgage broker.

Frequently Asked Questions

If my partner has owned property before, do we lose the first home buyer stamp duty concession?

In most Australian states, if your spouse or de facto partner has previously owned residential property, you are both disqualified from the stamp duty concession. Queensland is the only state that allows you to claim a concession on your specific share of the property interest.

What if I claim the concession, then I have to move for work before I meet the residency requirement?

Revenue offices monitor this closely and usually require you to repay the duty savings if you fail the residency test. However, if the move is due to unforeseen circumstances, some states have the discretion to reduce the penalty. The best course of action is voluntary disclosure to your state revenue office.

Does having my parents help (guarantor vs being on the title) affect first home buyer status?

There is a major distinction between a guarantor and a co-owner. If your parents are merely guarantors on the loan to help with serviceability, this generally does not affect your eligibility. However, if their names appear on the property title as co-owners, you may lose part or all of your first home buyer benefits.

I’m a permanent resident but not a citizen. Can I still get first home buyer duty relief?

Permanent residents are usually treated the same as citizens for standard stamp duty concessions. However, if you or a co-purchaser are classified as a foreign person for tax purposes, you may still be liable for a separate Foreign Purchaser Surcharge. This surcharge is often payable even if the base stamp duty is waived.

Summary

The difference between a full exemption and no eligibility at all is likely to be upwards of $20,000 in costs you need to budget for.

With some states only offering the brand to new builds you need to identify your target property early in the process so you know your budget.

With such significant variations state to state it is important you get some help early to assess your eligibility.

Get in touch with our team of expert brokers below to discuss your situation and we can do an eligibility check as part of a preliminary assessment.