First Home Owner Grants (FHOG) are used by state governments to encourage the development of new dwellings and increase the housing stock.

An eligible dwelling can be a house, townhouse, or an apartment. The only conditions being that it must be new, and below the state specific purchase price cap.

There are no grants currently available for existing housing.

However, the FHOGs are not to be confused with stamp duty exemptions. Which can be a huge concession for those looking to enter the property market.

In this article, we will provide a state-by-state breakdown of the grant amounts and price caps so you can assess your eligibility.

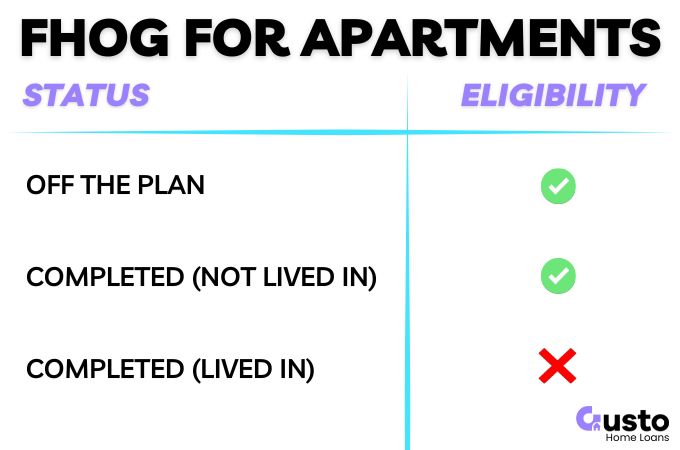

FHOG Eligibility: New vs Established Apartments

An apartment or unit can qualify for first home owner grants, but eligibility almost always comes down to whether it has been lived in before.

In most states, a property is considered new if you are the first owner.

This means it has not been previously sold as a residence or occupied by anyone, including the builder.

This is common for apartments bought through an off-the-plan contract, where you commit to a purchase before construction is complete.

Conversely, an established apartment that has been previously lived in will not typically meet the eligibility criteria.

Buying a one-year-old unit from an investor who rented it out means it is no longer a new home for grant purposes.

The same applies if you buy from a developer who first used the property as a display home.

It is also vital to understand there is no single, nationwide grant system.

Grant amounts and property value caps are not national and are set independently by each state and territory.

If you’re unsure whether a specific apartment counts as new under your state’s rules, our team of expert brokers can conduct an assessment on your behalf.

Click below to get in touch.

New Apartment Scenarios

For the grant, an apartment must be new, which typically falls into one of two scenarios.

Identifying which applies to you is the first step in confirming eligibility.

- Off-the-plan apartment: You sign a contract before construction is finished. Eligibility is typically tied to the contract price and it being the first sale of the property.

- Newly built but completed apartment: The building is finished, but the unit has never been occupied, sold, leased, or used for any short-term accommodation.

The rules also allow substantially renovated dwellings, but this usually requires structural changes, and not just cosmetic improvements.

This is very hard to achieve with an apartment.

To verify an apartment’s status, ask the agent or developer these direct questions:

- Has anyone ever lived in, leased, or used this unit for short-term stays?

- Am I buying from the developer (the first sale) or from a private owner?

- Is this a contract of sale, a building contract, or a combination?

State by State Guide to FHOG Amounts and Property Value Caps

The First Home Owner Grant is state-administered, so amounts and property value caps vary significantly.

The table below compares these grants for new apartments against median capital city unit prices (*as of Feb-2026).

| State/Territory | Grant | Eligibility | Price Cap | Cap. City Median* |

|---|---|---|---|---|

| NSW | $10,000 | New Dwellings | $600,000 | $903,000 |

| VIC | $10,000 | New Dwellings | $750,000 | $639,000 |

| QLD | $30,000 | New Dwellings | $750,000 | $824,000 |

| WA | $10,000 | New Dwellings | $750,000 | $699,000 |

| SA | $15,000 | New Dwellings | $650,000 | $666,000 |

| TAS | $30,000 | New Dwellings | No Cap | $576,000 |

| NT | $10,000 | New Dwellings | No Cap | $440,000 |

| ACT | – | – | – | $592,000 |

In markets like Sydney, where the median price is well above the cap, FHOG qualification becomes very difficult.

Finding a new apartment in the Greater Sydney area for $600,000 is nearly impossible, and in regional areas there will not be much new stock on the market.

The ACT removed their FHOG scheme in 2019, but the stamp duty concession is quite generous.

These rules change regularly so always check the specific rules for your state or territory before starting your search.

Other First Home Buyer Schemes

With new apartment prices exceeding FHOG caps it has become impractical for many new buyers.

However, there is still plenty of help out there for first home buyers who are looking to purchase a new or existing apartment.

Stamp Duty Concessions

If we stick with our NSW example, no stamp duty is payable on purchases up to $800,000.

While this is still lower than the median apartment price you will find plenty of apartments below this threshold.

Considering that stamp duty on an $800k purchase is just over $30,000, this is a huge help to aspiring apartment owners.

First Home Buyer Guarantee (FHBG)

The long standing FHBG scheme has been given a huge boost recently with the number of places now unlimited.

The price caps have also been changed to levels that few first home buyers are going to exceed.

For example, in NSW you are eligible for purchases up to $1.5 million.

Capturing the Full Benefit

Sticking with NSW, you can now purchase an apartment for $800,000 with a deposit of only $40,000.

No Lenders mortgage insurance or stamp duty payable.

Not a bad deal.

If by some miracle you can also find a new apartment for $600,000 or less then you can also qualify for the FHOG and receive another $10,000.

That last one is very unlikely though and I can’t image the scheme will remain in its current form for much longer.

Frequently Asked Questions

Does the First Home Owner Grant apply to an established apartment?

In all states that offer a FHOG, it is exclusively for new properties that have never been lived in or sold as a residence before.

When do I get paid the FHOG for an off-the-plan apartment?

Payment timing depends on how you apply. If you lodge through your lender, the grant is typically paid at settlement or when the first construction loan payment is drawn. If you apply directly to the state revenue office, payment usually occurs after the property is completed and registered in your name.

Can I rent out my apartment after I receive the First Home Owners grant?

All states require you to live in the property as your principal place of residence for a minimum continuous period, typically six to twelve months. Renting the apartment out before fulfilling this residency requirement is a big mistake and can result in you having to repay the grant in full.

Can I use the FHOG with the First Home Guarantee?

You can often use both schemes together, provided you and the property meet the eligibility criteria for each. They serve different purposes with the FHOG providing a cash boost for your deposit and costs, while the First Home Guarantee helps you avoid paying Lenders Mortgage Insurance (LMI).

Do studios or serviced apartments qualify for the FHOG?

This depends on two separate checks. First, the property type must meet your state’s definition of a home for grant eligibility. A studio should qualify, a serviced apartment would not. Second, your lender must accept the property as suitable security for a home loan.

Summary

Apartments qualify for the First Home Owner Grant if they are new and priced within your state’s value cap.

The critical factor is new versus established, not the dwelling type.

Check your state’s cap against your target apartment price, and don’t forget stamp duty concessions often provide bigger savings.

For a free consultation on your eligibility for the FHOG, or other government schemes get in touch with our team below.