While the standard mortgage term in Australia is 25-30 years, most home loans are refinanced between the 3-5 year mark.

The market is always shifting, and as your equity position and finances improve, then better mortgage options often become available.

You can lock in significant savings by refinancing to a better interest rate, and this really compounds over decades until you fully repay your mortgage.

But how long should you wait before you refinance your house?

The answer will depend on the savings available to you and how much work you are willing to do to get them.

In this article, we will discuss when it can make sense to refinance as soon as you can, and when you will be better off waiting a little longer.

What is the Minimum Time Before You Can Refinance?

There’s no legal minimum timeframe for refinancing a home loan in Australia. Technically, you could do it the next day.

For most, settlement is such a big relief and the idea of revisiting all that paperwork so soon is the furthest thing from their mind.

There are some rare cases where the benefits are so significant that a homeowner may choose to refinance within a few months.

For example, a lender offering a very low rate, or huge cash back incentives, could be motivating enough to go through the process again.

But you always need to offset this with the switching costs.

So while you can refinance at any time, whether you should depends on whether the time, effort, and the savings stack up.

Implications of Refinancing Straight After Settlement

Ever since the government banned mortgage exit fees in 2011, it has been much easier to refinance.

However, there are still plenty of costs involved when refinancing that a borrower should quantify before making the decision to move lenders.

Refinancing a Fixed Interest Loan Early

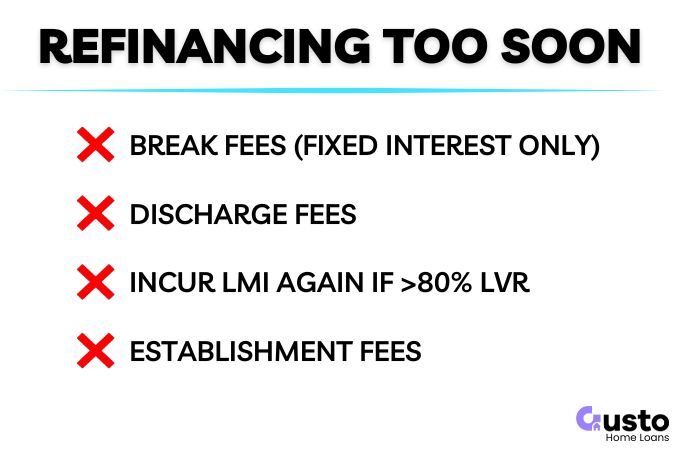

Fixed interest loans are notoriously costly to refinance, especially if interest rates have fallen since you locked in your fixed rate.

This is due to break fees, which are a function of the time remaining in your fixed term and the difference in current market rates.

If you are refinancing soon after settlement then the second half of that equation is as long as its ever going to be.

In most cases, it just isn’t worth refinancing while in a fixed rate period.

Learn more about break fees here.

Refinancing a Variable Interest Loan Early

Variable-rate loans are far more flexible, and refinancing shortly after settlement may be palatable for the borrower.

There will still be costs involved in discharging your mortgage and establishing the new loan.

But if you can save a lot of money long term then it will make sense to do.

Impact of LMI (Lenders Mortgage Insurance)

If you have borrowed more than 80% of the value of your home then you have probably just paid a chunky LMI bill.

Refinancing immediately after settlement is most likely going to mean paying this again.

Considering the LMI for an average mortgage in Australia is north of $10,000 it can be prohibitive to incur this again.

You may be able to avoid this if:

- Property values are increasing rapidly in your area and a higher valuation reduces that loan-to-value ratio (LVR) to <80%.

- You have recently come into money that would allow you to reduce your total borrowings and reduce that LVR.

- You qualify for an LMI waiver with your new lender, which is possible with some professions.

Fees to Consider When Refinancing Early

In addition to the loan specific switching costs we have covered so far, you will also be up for a range of standard fees:

- Loan discharge fee

- Mortgage registration fees

- New lender application or establishment fees

- Any valuation fees

As you can see, you need to be thorough when quantifying the cost of refinancing within a short timeframe as these costs add up.

Broker Clawbacks

While this is not a cost to the borrower, it certainly is a cost to a mortgage broker who has assisted you in setting up the original mortgage.

Mortgage brokers get paid by the lender when your loan settles, which keeps their services free for the borrower when dealing with residential property.

However, if you refinance within 12-24 months the broker is going to be liable to pay any commissions earned back to the lender via a clawback.

A broker cannot pass on this cost to you according to Australian regulations.

When You Should Refinance Early

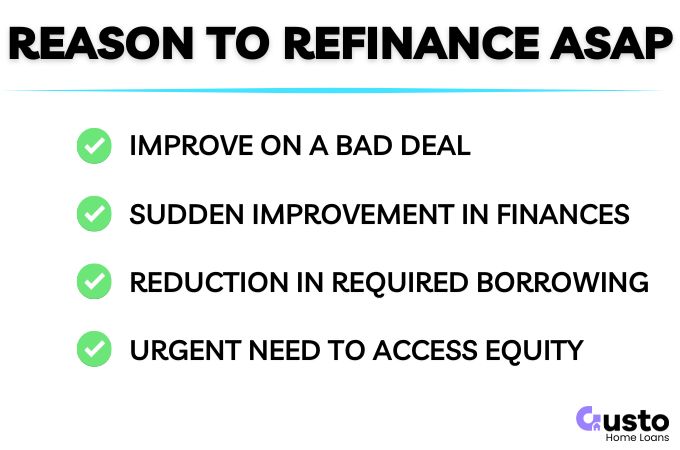

There are scenarios where refinancing early makes financial sense, but this would normally follow a big change in life circumstances, or a poor experience setting up your initial mortgage.

You Got a Bad Deal

Perhaps you went straight to a bank and have only just discovered what a mortgage broker can do for you.

Or you dealt with a broker who just wasn’t very good… and therefore deserves the clawback if their work is costing you money!

However you got here, if you are now in an expensive mortgage it will be worth your time to refinance ASAP if there are better options available.

If you are not sure, and you would like a second opinion on your current rate and alternative options then click below to get in touch with our expert team.

Your Financial Circumstances Have Improved

Sometimes you need to accept a higher interest rate so you can secure a loan approval, because that is the only lender where you qualify.

But things can change rapidly on the lender and the borrower’s side.

If industry credit policies have become more favourable then perhaps there are cheaper mortgage options now available to you.

On the borrower side, an unexpected pay increase, or windfall of cash that could reduce borrowings, may also increase the number of good lender options available to you.

When you can access a lower rate that will save you a sufficient amount of money for the refinance to be worthwhile, you should do this as soon as you can.

Regardless of how long you have been in your current mortgage.

You Want to Release Equity

The path of least resistance is usually to approach your current lender about releasing additional equity.

However, if you have reached the limit for what they will lend you then you may have to consider alternative options where a higher limit may be possible.

You will also need to have sufficient equity to support the additional borrowings, and ideally being able to do so without incurring LMI.

However, this may also depend on how urgent the need is for the extra cash.

When You Should Not Refinance Early

Refinancing too soon can often be too costly for it to be worthwhile. Unless you are able to access various incentives such as cash back, or a honeymoon interest rate.

Our brokers will always advise you to wait in the following circumstances.

Switching Costs Are Too High

The accumulated fees for discharging your existing mortgage, and establishing your new loan, may outweigh the benefits of refinancing.

Even if you will save money, the timeframe to recoup the costs also needs consideration.

If it takes five years to come out ahead but you plan to sell in 2-3 years then it may not be in your best interests to switch.

Our brokers will always do a thorough comparison so you know exactly where you stand before starting a formal application.

Your LVR Is Above 80%

A high LVR will mean that you could be liable to pay LMI again.

If you were to wait for the property value to appreciate while you also pay down the principle over time, then you could be in a much better position to refinance later on.

You may also have more lender options once your LVR comes down. Which means a better outcome all round.

Your Financial Situation Has Declined

A lender can only assess a mortgage application based on your current financial capacity.

A negative change to your income, such as job loss, change in employment, or extended sickness, will make it more difficult to be approved for a refinance.

If you have taken on additional debt since your mortgage was settled this would also be a limitation.

You may need to wait until new loans are paid out, but it all depends on the type of debt and how much your repayments are.

Summary

If you can save money by refinancing your home loan, and you are likely to be approved, then you should so it as soon as you are able.

Even small savings on your interest rate can add up to thousands over a 30 year loan term!

A cheaper mortgage also gives you freedom of choice. You can put money back in your pocket, or maintain higher repayments and be debt free sooner.

As discussed in this article, there are a lot of variables to consider to determine if the savings are genuine over the long term and in your best interest.

Our team of brokers can run the calculations for you so you know where you stand, and what your current options are in the mortgage market.