As part of your home loan application a lender will want to scrutinise your bank statements so they have your complete financial circumstances.

This is done to ensure that there is truth in your declared income and expenses, while also looking for other clues into your risk profile as a borrower.

Most mortgage lenders will look at 90 days worth of statements.

But what exactly are they looking for?

In this article, we’ll discuss how lenders use digital categorisation to verify income, map expenses, and hunt for undisclosed liabilities.

We’ll also cover the high risk transactions that can see your application rejected, even if you can afford the loan.

Verifying Your Declarations

Lenders have a legal obligation to verify all of your financial infomation that is declared when you submit a home loan application.

Your bank statements are a fast track to sort through a lot of data in quick time using digital categorisation, and comparing to your declaration.

Brokers complete the same process prior to the formal submission.

So, if you would like to have some expert eyes on your statements before committing to an application get in touch with our expert team below.

Income

Mortgage lenders will look at your deposits to confirm the regularity, source, and net amount of your income credits.

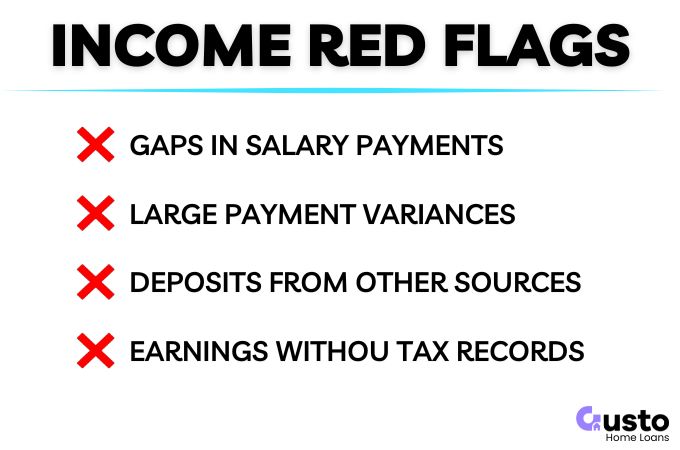

Lenders will flag account activity that does not tell a consistent story. The following scenarios will trigger additional questions during a credit assessment:

- Unexplained employment gaps or irregular pay cycles.

- Fluctuating deposit amounts.

- Large one-off deposits that look like income.

- Side-hustle earnings from rideshares or online marketplaces that lack supporting tax returns.

Your payslips and possibly an employment letter will be an important reference for your annual earnings.

Especially if you work overtime, or receive bonuses, as part of your salary package.

If your deposits are not consistent with the expected amounts then you should be prepared to explain the variations.

Expense History

A lender will build a month-by-month picture of your inflows versus outflows to verify whether you can comfortably afford the new mortgage repayments.

This calculation will differ between lenders, but most will require the mortgage repayment plus a buffer so that you can absorb changes in your finances without falling behind.

Some red flags could be if your account balances regularly drop near $0 before payday, and frequent account-to-account shuffling to make it through the week.

The opposite is a more positive pattern for a loan assessor.

A stable end-of-month savings buffer and a predictable, automated bill cadence.

If you keep your account balance stable and regimented with your expenses then it looks like a well managed budget.

Just be mindful that slashing your expenditure to bare bones may not actually boost your borrowing power.

There is a floor on the expenses a lender will use in a serviceability calculation to ensure the financial picture is reasonable and sustainable.

Most lenders use a version of the Household Expenditure Measure (HEM) to determine what the floor should be.

If your spending falls below this benchmark, the bank simply applies the higher HEM figure.

So it is best to be transparent with your declarations.

Debt Repayments and Credit Limits

If you have other debts that are on a fixed repayment schedule then this is easy for the lender to factor into your income and expenses.

However, if you use credit cards or other limit based loan products then a lender will calculate your exposure based on what you could borrow, not just what you owe today.

A credit card with $0 owing, but a $10,000 limit, will be calculated at the $10,000 level.

Usually applying a 3%-4% minimum repayment, which will reduce your free cash available for loan repayments.

So if you need to maximise your borrowing capacity it may be worth reducing your unused credit limits.

Or if you no longer need it, closing the facility completely.

How Buy Now Pay Later Affects Your Approval

BNPL complicates things further and can lead to you being overly penalised in your repayment capacity calculation.

You may only have two repayments left to clear your balance, or you could be a habitual user of these services.

Mortgage lenders are going to take a conservative view and may just assume the payments you are making today will go on forever.

Which can reduce your borrowing capacity by tens of thousands of dollars.

As a general rule, when a lender sees you regularly engaging in short term credit it is not a positive factor.

Higher risk behaviour that could lead to a rejection can include:

- BNPL used for daily essentials like groceries.

- Multiple active BNPL accounts.

- Constant repayments across every pay cycle.

- Stacking BNPL with other personal debt.

The good news is that if you stop engaging with these services you can be free of the debt within a couple of months.

High Risk Transactions

The following are some of the red flags that lenders will look for that can increase your risk profile considerably.

Payment Reversals and Overdrawn Fees

An overdrawn account could lead to an instant rejection depending on the lender.

It indicates poor management of finances and a lack of surplus cash to support a new mortgage.

The associated fees are wasteful, and there could also be arrears accumulating on various bills or debts that will need to be factored in.

Avoid the following transactions in your bank statements:

- Overdrawn balances

- Repeated penalty fee charges

- Dishonoured direct debits

- Late repayments on current loans or credit cards

Frequent Gambling Related Transactions

While a bet here and there is fine, excessive and frequent gambling is a strong indication that you are not managing your money well.

A deposit into an online bookies account is easy to spot, but beware of frequent ATM withdrawals also.

If they are in a licensed venue, or are made in high frequency, they may be classified as gambling transactions too.

The best solution here is to avoid all gambling transactions for a few months leading up to your loan application.

Payday Loans

Relying on short term cash loans to make ends meet is another indication that your budget may not be in good shape.

Every time you apply for a loan there is a mark left on your credit file that will be visible to other lenders for up to five years.

This happens regardless of whether you are approved for the loan or not.

A lender will know if you have engaged in this type of borrowing in the past, even if it is not visible on your bank statements as a current loan.

They are high cost loan products and you should stop using these well in advance of applying for a home loan.

Unexplained Deposits

A sudden $10,000 deposit might seem like a win, but to a mortgage lender, it could indicate hidden borrowing or more nefarious things.

Lenders do not dislike extra cash in your account, but if there is no paper trail it raises suspicion.

Assessors must rule out undisclosed debt, unacceptable income sources, and anti-money laundering risks.

You can prevent these transactions from stalling your loan by proactively explaining the money.

Some common reasons for these deposits could be:

- Gifts: Provide a signed gift letter alongside a clear bank transfer trail.

- Private Sales: Supply a simple bill of sale and a matching deposit entry.

- Cash: Physical cash always attracts heavy scrutiny. Prepare a clear written explanation before submitting your application.

How Automated Tools Calculate Your Living Expenses

Lenders use digital categorisation tools to instantly ingest and analyse your transaction history.

These systems automatically group your spending into specific living expense categories.

This software easily spots transaction patterns that reveal undeclared dependents or hidden financial commitments.

Regular payments for childcare, school fees, or recurring transfers to family members will immediately flag in a lender’s system.

Automated categorisation is built to detect inconsistencies, so you should never try to game the system.

Instead, you need to prepare your application properly:

- Declare your dependents and major recurring costs accurately from the start.

- Keep a clear explanation ready for any regular account transfers.

- Maintain total transparency with your broker to avoid triggering manual reviews.

Bank Statement Clean-Up

No matter your current situation, you can achieve a lot in 90 days prior to applying for a home loan.

A messy financial profile can present as a well organised budget with some very basic changes maintained over time.

Cut out any unnecessary expenses that may be reducing your cash buffer, such as unused streaming services or subscriptions.

Payout any debt that is short term, or low balance, to get the transactions out of your statements.

Abstain from any gambling or other high risk transactions.

In just a couple of months you will be in better shape and will have saved a ton of money.

Frequently Asked Questions

How many months of bank statements do lenders require?

Most lenders require three months of transaction history for everyday accounts. Self employed borrowers or complex applications may require six months of records. More complexity simply requires a longer paper trail.

Will a one-off expenses lead to my mortgage application being rejected?

A single expensive purchase will not ruin your approval. Credit assessors focus on your ongoing commitments and regular savings buffers rather than isolated events. One off splurges rarely impact your borrowing power.

Can I stop spending for a month to get approved?

Sudden drops in your living expenses will raise red flags. Lenders prefer consistent financial behaviour. Declare your true living costs accurately and let our brokers find a suitable lender for your lifestyle.

Do joke bank transfer descriptions affect my home loan application?

It depends on the content, but yes it can. Silly transfer descriptions can trigger further questions form the lender and delay a final decision. Keep your transaction descriptions neutral and be prepared to clarify past jokes if asked.

Getting Your Bank Statements Ready

Your bank statements should align with your declared income and expenses in your home loan application.

The review should reveal nothing further to increase your risk profile so that you have a smooth pathways towards loan approval.

Even if you have had some poor habits in the past, you can tidy these up in a couple of short months and remove the friction you would otherwise encounter.

If you would like a preliminary assessment of your bank statements and home loan prospects then get in touch with the Gusto team below.

We will match you with a lender whose credit policy fits your transaction profile, eliminating surprises and ensuring a fast approval.