When you apply for a home loan the lender will assess your budget to determine what cash flow is available for your new mortgage.

However, this will always be much lower than your actual spending would suggest.

This can frustrate borrowers who can clearly afford mortgage repayments on paper but the bank says otherwise.

So, why does this happen?

One big reason is that lenders apply an interest rate buffer in addition to the actual mortgage rate that will be charged on the loan.

This is to stress test the borrower’s finances in the event of future interest rate increases.

For some lenders this is a regulated requirement, others do it as a risk mitigation measure.

In this article, we will explore the mandatory buffer that all APRA regulated banks, and how that impacts your loan serviceability assessment.

What is the APRA Serviceability Buffer?

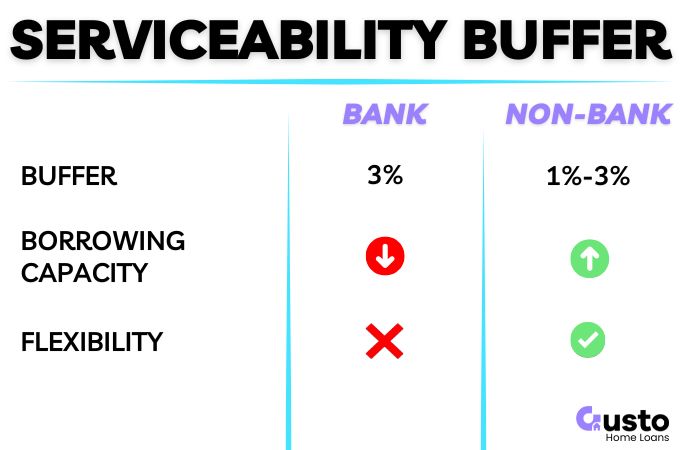

The APRA serviceability buffer is a mandatory interest rate margin (currently 3%) added to the existing rate to assess your repayment capacity.

For example, if your bank offers a 6% interest rate and the buffer is 3%, the bank tests your finances as if you are paying 9%.

Your maximum borrowing amount will be lower as a result, and your household budget is (theoretically) more able to absorb any future changes in your circumstances.

Why Does it Exist?

APRA is responsible for regulating the banking system and one of the biggest risks to that system is large scale defaults on mortgages.

Australian banks hold huge mortgage loan books and is a primary driver of profits for most of the largest financial institutions.

The buffer ensures that borrowers are not being stretched beyond their limits on the day they take out their new mortgage.

Which de-risks these mortgage books significantly throughout the banking system.

Who Does this Apply To?

APRA regulations only apply to Authorised Deposit-taking Institutions like banks, credit unions, and building societies.

Non-bank lenders operate under different rules.

While ASIC requires them to lend responsibly, they are not bound by APRA’s rigid prudential expectations.

So, they have more flexibility when setting their credit assessment policies.

The result is that you can get vastly different outcomes for the same customer depending on which lender you apply with.

This is one reason why it is important to use a broker who can match you with the lender that best fits your objectives and your credit profile.

However, flexible lending does not mean zero checks. Alternative lenders still rigorously verify your income and living expenses.

They simply apply their own internal serviceability buffers to ensure you can safely manage the loan.

How Your Borrowing Capacity is Assessed

To determine your maximum borrowing capacity, lenders generally test four main inputs:

- Total income

- Existing debts

- Number of dependants

- Living expenses

They calculate your mortgage repayments using a higher assessment rate.

This combines your product rate with the APRA serviceability buffer to prove you will maintain a cash surplus if interest rates rise.

Lenders also enforce a floor rate. This is an absolute minimum percentage used to test your finances, even if your rate plus the buffer is lower.

Because institutions use different internal floor rates and expense models, your borrowing power fluctuates.

What to Do if the APRA Buffer Prevents Approval

The interest rate buffer is just one element that contributes to your overall serviceability calculation.

There is a range of other factors that can also significantly affect the outcome, that will differ between lenders.

Placement with the right lender could mean approval in spite of the APRA buffer, or potentially avoiding it altogether.

Some examples include:

- Income shading (only a portion of income used in calculation).

- Inflated living expenses.

- High credit card limits even when outstanding balance is low.

- Aggressive expense assumptions.

A good broker will spot these issues long before a formal application is submitted and only direct your application where the credit policy is most favourable.

Frequently Asked Questions

Is the APRA serviceability buffer still 3%?

Yes, the APRA serviceability buffer remains at 3% as of early 2024. APRA regularly reviews these macroeconomic settings and can adjust this figure up or down depending on market conditions. Keep in mind that individual banks can always choose to apply a higher internal buffer to protect their own lending portfolios regardless of the APRA baseline.

Does the 3% buffer apply to investors and interest-only loans?

Yes, the buffer absolutely applies to property investors. Interest-only loans actually face even stricter assessments. The bank calculates your repayment capacity based on the shorter principal and interest period that follows your initial interest-only term. As a result, your maximum borrowing power will be much tighter compared to a standard owner-occupier mortgage.

How does the buffer affect ‘like-for-like’ refinancing?

Refinancing becomes much harder after consecutive cash rate rises because the overall assessment rate jumps significantly. Some lenders offer limited discretion for a like-for-like refinance and may apply a reduced 1% buffer under very strict conditions. Always check with our broker first.

Do non-bank lenders ignore APRA’s buffer?

Non-bank lenders are not Authorised Deposit-taking Institutions, so they are not bound by APRA guidelines. They still must lend responsibly under ASIC rules and use their own internal serviceability calculations.

Can I improve my serviceability without earning more money?

Sometimes you can improve serviceability by selecting a lender who’s credit policy is more favourable to your personal circumstances. However, you can also increase your borrowing capacity by reducing your existing financial liabilities. Lowering credit card limits, paying off personal loans, and potentially reducing discretionary expenses.

Summary

The APRA serviceability buffer is a 3% stress test used to assess your loan affordability, not your actual interest rate.

However, this mandatory margin can severely reduce your borrowing power or block a refinancing application, even if you always pay on time.

Fortunately, approval outcomes vary widely between lenders.

One major bank might decline your application, but an alternative lender could approve you based on different buffers, income treatments, and living expense models.

Before you lodge a formal application, you need to know exactly where you stand.

The team at Gusto Finance can run a free serviceability check and model your scenario across multiple lenders.