Borrowers have an abundance of choice when shopping for a mortgage and it can be a lot of work to find the best deal for you.

However, what you won’t know is what happens in the background when assessing your application.

You may think you are a high earner, and a strong applicant, but your income just doesn’t fit a lender’s policies and you are declined.

This is just one of many reasons a lender may look at your profile differently than you assume.

A broker has access to these policies for a whole range of lenders and can match you with the one that is the cheapest, and provides the most favourable assessment.

In this article, we’ll look at 11 reasons why a broker can get you a better result (often for less work) than going directly to a lender.

All for zero cost to the borrower.

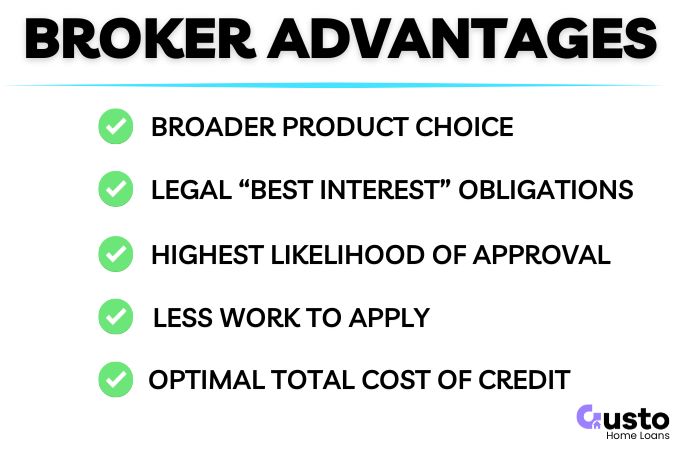

Comparing Brokers and Mortgage Lenders

Your lender choice can save you thousands over the life of your mortgage.

These highlights summarise the core differences between brokers and banks.

- Wider Choice: Banks only sell their own products where a brokers will compare dozens of lenders to find the most competitive fit for you.

- Legal Protection: Australian brokers must legally act in your best interests. Banks are not bound by this same legal duty.

- Higher Approval Odds: Brokers match your profile to specific lender policies to improve approval odds for unconventional incomes or small deposits.

- Streamlined Process: You provide documentation once. Your broker manages the lender negotiations and administrative hurdles through to settlement.

- Balanced Value: Direct lenders can be cheaper for simple loans, but brokers ensure you do not trade flexibility for a low headline rate.

1. Legal Protection Banks Don’t Offer

In Australia, brokers are legally bound by the Best Interests Duty (BID).

This mandate requires brokers to prioritise your financial goals over their own.

They must recommend the most suitable product for your needs, not the highest-paying or easiest option.

A bank employee has no such obligation, and cannot provide this protection regardless.

They act as salespeople for one brand and cannot recommend a competitor, even if that lender offers a lower rate or better features.

Their job is to sell their employer’s products regardless of whether a better deal exists elsewhere.

To demonstrate this, a broker will complete a preliminary assessment and document the following:

- Interest rates and annual fees

- Specific loan features

- Policy fit for your situation

2. Broker Access to More Lenders Will Change Your Outcome

A bank offers exactly one credit policy and one product suite. If your financial profile falls outside their narrow criteria, they simply decline the application.

Brokers provide access to a panel of major, non-bank, and specialist lenders.

This ensures your application is matched to a lender whose rules align with your specific circumstances.

Wider choice unlocks competitive pricing and flexible features a single bank cannot match.

Different lenders have varying appetites for specific scenarios:

- Alternative servicing models that better handle HECS debt

- Niche products for self-employed or investment-focused borrowers

- Generous assessments for bonus income or rental yields

A quality broker should provide a mix of major, non-bank, and specialist lenders to maximise your borrowing power and pricing options.

3. Varied Income Assessment Methods

A bank decline is often the result of a calculation of your borrowing power that is specific to that lender.

Lenders can assess the same borrower differently based on:

- Income shading (e.g., only counting 80% of rental income).

- Treatment of overtime, bonuses, or commissions.

- Benchmarks for HECS debt or existing investment loans.

Brokers understand these varied policies and match your profile to the lender most likely to provide an optimal income assessment.

It is important to be transparent with your broker and to disclose non-standard details early so your broker can identify the right lending option early.

4. Comparing the Total Cost of Credit

The lowest interest rate doesn’t always equal the cheapest mortgage when you add up all the related costs.

Many borrowers are sucked in by honeymoon rates that spike after a year or professional packages with high annual fees that negate interest savings.

These have their place if you are utilising the full benefits and understand how it affects the long term cost structure,.

A broker helps calculate the total cost of ownership as part of the initial market comparison so you can make an informed choice early.

This includes:

- The interest rate

- Ongoing and discharge fees

- Features like offset accounts, redraw, or split loans

A slightly higher rate with an offset account often saves more over time than a restrictive basic loan.

5. Reducing the Admin Burden of Your Application

While most lenders require similar documentation when applying for a mortgage, their formatting conditions and criteria vary.

One bank may accept a digital payslip, while another requires a signed letter from your employer to verify your income.

A mortgage broker removes this administrative friction.

You provide a single document pack and they handle the rest.

They package your application to meet specific lender expectations and manage all follow-ups with the credit department, saving you hours of tedious back-and-forth.

This keeps the application moving without you having to play middle-man with the lender.

6. Speed to Loan Approval

Approval times fluctuate based on a lender’s backlog, the time of month, and loan complexity.

Brokers understand which pathways are currently moving fastest and what the expected timeframe would be with each lender.

Other causes of delay include:

- Lenders Mortgage Insurance (LMI)

- On-site property valuations

- Specific conditional requests

- Missing information or documents

A broker’s advantage is live market knowledge.

While a major bank may have a 14-day queue, a non-bank lender might offer 48-hour turnarounds.

Selecting the right lender for your scenario prevents rework and protects your contract dates.

7. Why Your Broker Is Your Best Backup Plan

Going directly to a bank creates a single point of failure.

If they reject your application, the deal often collapses.

Common hurdles that trigger bank rejections include:

- Low property valuations

- Unexpected loan conditions

- Sudden policy shifts

- Sudden change in borrower circumstances

- Flagged property types

A broker treats a no as a pivot point.

Since they already hold your full file, they can quickly redirect your application to a backup lender with a different risk appetite.

This agility ensures that one lender’s internal shift does not ruin your purchase.

8. How Ongoing Support Defeats the Loyalty Tax

Many borrowers suffer from a loyalty tax where lenders offer new customers aggressive discounts while existing ones drift onto uncompetitive rates.

Your broker provides post-settlement value by managing regular pricing requests, challenging your lender to match their sharpest market offers without moving banks.

They also track fixed rate expiry dates to prevent rate shock before you revert to variable pricing.

This strategy ensures your mortgage stays competitive long after the excitement of settlement fades.

Where your current mortgage falls behind the market in terms of value, you can refinance to another lender with your broker to lock in additional savings.

9. Structuring for the Future

Banks often treat property portfolios as liabilities by shading rental income by 20%, capping your borrowing power.

A broker identifies lenders with flexible interest-only policies and ensures properties remain standalone.

This prevents messy cross-collateralisation that puts your family home at risk if an investment property underperforms.

Upgraders face significant pressure regarding buy-sell timing and bridging costs.

Brokers coordinate a seamless transition by:

- Arranging cost-effective bridging finance

- Negotiating extended settlements to align dates

- Using existing equity to maximize your budget before listing

The more information you share with your broker the better they can set you up for future success.

10. All the Benefits, Zero Cost

Brokers generally offer their services at no cost to you because they are compensated by the lender.

This includes an upfront commission on the loan and an ongoing trail commission for the life of the mortgage.

This model keeps professional advice free for most residential borrowers.

11. Personally Invested in Your Success

A mortgage broker is more likely to maintain an interest in your financial progress over the long term.

Even large brokerage firms are likely to have a single person managing your applications over many years.

Compared to the experience dealing with a broker directly and you will rarely speak to the same person twice on the same application.

The personal service and vested interest in providing an outstanding service now, and into the future, is a huge part of the value offered by a broker.

Frequently Asked Questions

Can going direct to a bank or digital lender be cheaper?

It can be for simple borrowers with large deposits. Some digital lenders offer lower headline rates by removing broker commissions from their model. However, you must calculate the total cost of ownership, including annual fees and loan flexibility. A broker often finds offset features or tax effective structures that outweigh a lower rate from a direct lender.

How do I check a broker is acting in my best interests?

You can verify this by requesting a written Credit Proposal. This document compares different lenders and explains why the recommended loan is the most suitable for you. Under the Best Interests Duty, brokers must legally prioritise your financial goals. Always check for their Australian Credit Licence and a clear disclosure of the commissions they will receive.

Is a mortgage broker really free in Australia?

Yes, for most residential borrowers. Lenders pay brokers a commission once the loan settles, which keeps the service free for you. Exceptions may apply for complex commercial deals or very small loans where an additional fee might be charged. Any such fees must be disclosed in writing via a Credit Quote before you start the process.

How to Choose the Best Path to Your Home Loan

The most important question to ask yourself is how much work you want to do as part of the mortgage application process.

If you want to shop around and get into the details of all the mortgage products offered across the market, and also manage the application process, then direct to the lender may suit.

If you want instant access to a full panel of lenders, and want to outsource much of the calculations and application preparation, at no cost, then a broker can be the best option.

For those who are also looking for insight into long term planning and structuring of your finances then a mortgage broker can help long before you commit to a formal application.